This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Many of us are covered by one or more types of defined contribution retirement plans, such as a 401(k), 403(b), 457, or any of a number of other plans. What many of these plans have in common is that they are referred to as Cash Or Deferred Arrangements (CODA), as designated by the IRS. So, what should you do about this?

Employers have the discretion to opt out of permitting 83(i) elections by declining to establish these conditions or explicitly excluding the election from equity compensationplans. This ensures employers maintain control over the application of 83(i) elections within their equity compensationplans.

It’s common for businesses to court talented executives with a variety of perks, including signing bonuses, stock options, and nonqualified deferred compensationplans to supplement regular pensions and retirement savings.

Deferred CompensationPlans Nonqualified Deferred Compensation (NQDC) plans allow high-income earners to defer a portion of their income to a later date, such as retirement, when they may be in a lower tax bracket. Harness Tax LLC is affiliated with Harness Wealth Advisers LLC, collectively referred to as “Harness”.

As of October 9, 2024 If your firm provides comprehensive tax planning services, you’ll be better positioned to gain new clients in the Harness Marketplace compared to firms that mainly focus on tax preparation. The form will collect detailed information about your tax practice, including: How is your firm and team structured?

Income Reduction : Your employer may offer a deferred compensationplan that allows you to postpone approximately 10% of your salary or a bonus. Reduce Taxes on Capital Gains : If you make money from selling an investment, you must pay a tax from those gains, also referred to as the capital gains tax (CGT). Growing tax deferral.

The intent of stock option compensation is to align the interests of the employees with that of the company: The employee’s compensation increases as the stock price increases. Stock options can be either qualified or non-qualified, and the primary difference is how they are taxed.

Qualified small business stock (QSBS) Qualified Small Business Stock (QSBS) refers to shares in a corporation that meets certain criteria set by the Internal Revenue Code. Health Savings Accounts (HSAs) HSAs are available to individuals enrolled in high-deductible health plans (HDHPs). Get started with Harness today.

Microsoft Technology Licensing, Undead Labs The Microsoft 401(k) plan is part of the comprehensive benefits offering that includes the Microsoft Corporation Employee Stock Purchase Plan and the Microsoft Corporation Deferred CompensationPlan. Getting the full match is like a nearly 7% raise on a $150,000 salary!

What’s the Risk of the Intel SERPLUS Plan? As a non-qualified deferred compensationplan, your SERPLUS account is, by rule, an unsecured liability of Intel. This is the primary risk and the main drawback of participating in the deferred compensationplan. IBM is also shown for reference (See chart below).

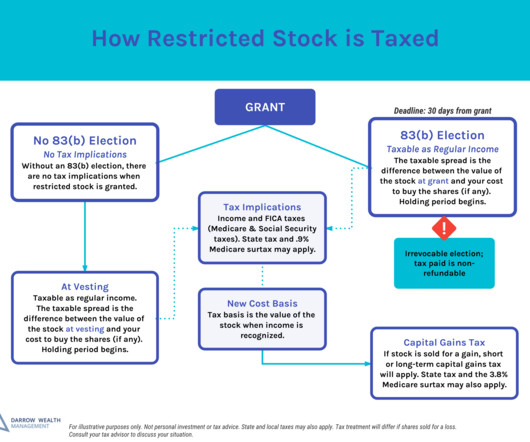

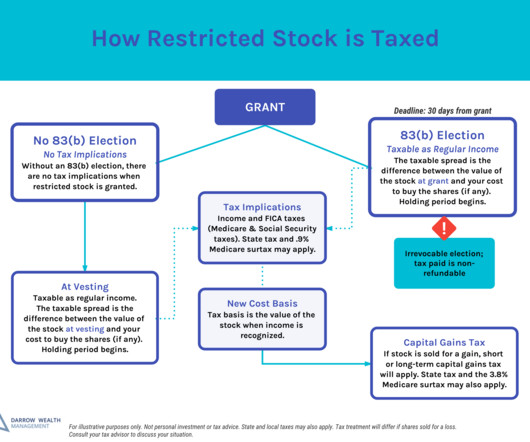

A restricted stock award (RSA) is a form of equity compensation. RSA grants are commonly issued by private companies, particularly early-stage startups, and may be referred to as founder’s stock or simply restricted stock grants awarded to employees.

A restricted stock award (RSA) is a form of equity compensation. RSA grants are commonly issued by private companies, particularly early-stage startups, and may be referred to as founder’s stock or simply restricted stock grants awarded to employees.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content