This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

"How much can I spend in retirement?" is perhaps the most fundamental question a client brings to their advisor. Advisors want to help clients set a secure, reliable retirementplan, yet even the most comprehensive assumptions will inevitably deviate from reality at least to some degree.

RIAs can create a potential client stream if they commit to a 401(k) channel that includes participant education and touchpoints, said panelists at Wealth Management EDGE last week.

Mason received a 97-month prison sentence for defrauding clients of over $17 million. Mason, a former advisor who was barred from the industry, was sentenced to 97 months in prison and three years of supervised release for defrauding at least 13 advisory clients out of more than $17 million, according to the Department of Justice.

These services may range from 'standard' offerings like retirementplanning to less traditional areas like credit card consulting. In a firm's early years, there tends to be more room for experimentation, with advisors adding new services to provide value and attract clients.

This lack of clarity made retirementplanning significantly more challenging. As a result, it's important for advisors to first identify which clients are currently subject to WEP or GPO and ensure that those who may need to file for benefits do so as soon as possible. Read More.

But as more individuals confront the emotional realities of this life transition, many find that the absence of structure, socialization, and identity once provided by work can create a gap that traditional retirementplanning doesn't fully address. While the core elements of traditional retirementplanning remain (e.g.,

For many financial advisors, a core part of the retirementplanning process involves simulating whether the client's assets will last through retirement. Yet while these tools offer mathematical metrics, they often fall short in helping clients connect the numbers to their real lives.

Solo 401(k) plans are a popular retirement savings vehicle for self-employed business owners. By maximizing both the employee employer contributions, solo 401(k) plan owners can often save significantly more than is possible with other types of retirementplans available to self-employed workers, like SEPs and standard IRAs.

Which will ultimately provide greater tax planning certainty to advisors and their clients for 2025 and beyond (and avoid the year-end rush they faced with the late-December passage of TCJA in 2017).

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that a recent report finds that the number of SEC-registered RIAs, the assets that they manage, and the number of clients they serve all increased between 2023 and 2024 and suggests the industry is robust across the size spectrum, (..)

Advisors have a relatively brief window of time to communicate their value to prospective clients. In this article, Senior Financial Planning Nerd Sydney Squires draws on research from Morningstar that identifies 11 core motivators that influence how prospects choose their particular advisor. Read More.

For financial advisors helping clients prepare for retirement, understanding and planning for the costs associated with Medicare is critical. While these costs are often lower than those incurred through pre-65 health insurance, they remain significant, especially when viewed over a multi-decade retirement.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with a recent survey indicating that a majority of advisors are viewing new client acquisition as their primary challenge in the current competitive environment for financial advice (followed by compliance and technology management) and suggests (..)

In the early days of financial planning, serving clients often meant developing transactional relationships focused on facilitating trades and selling insurance. Over time, advisors shifted toward more analytical approaches, such as investment management and retirementplanning.

Enjoy the current installment of "Weekend Reading For Financial Planners" – this week's edition kicks off with the news that at a time when brokerage firms' cash sweep programs come under increased scrutiny (and as the Federal Reserve has cut interest rates), Charles Schwab (the largest RIA custodian) continues to slash sweep rates for client (..)

The Diamond Podcast for Financial Advisors: 10 Ways Top Advisors Are Growing Their Businesses The Diamond Podcast for Financial Advisors: 10 Ways Top Advisors Are Growing Their Businesses A “Top 10” list of firm-level innovations and grassroots methodologies from some of the most successful advisors, teams and firms in the business.

Which could prove to be a boon for the financial advice industry as more consumers are willing to entrust their assets to an advisor (while at the same time possibly making it tougher for some advisors to differentiate themselves primarily by how they put their clients' interests first?). Read More.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement.

When onboarding new clients, financial advisors often use a three-meeting cadence: a Discovery Meeting to gather information, a Presentation Meeting to discuss the plan, and an Implementation Meeting to finalize it. while also setting the tone for a long-term planning relationship built on trust and deeper client engagement.

Seth is the founder of Heartwood Financial Planning, an advisory firm affiliated with PlanMember Securities Corporation that is based in Fresno, California, and oversees approximately $100 million in assets under management for 850 client households. My guest on today's podcast is Seth Scott.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that according to a recent study by DeVoe & Company, only 42% of RIAs surveyed have written succession plans and either have begun to implement them or have already done so.

These results largely match results from the recent Kitces Research Study on Advisor Productivity, which found that the typical fee schedule for firms charging on a graduated basis remains at 100 basis points (bps) for client assets up to $1 million, then declines to 90 bps at $2 million, 75 bps at $5 million, and 60 bps at $10 million in assets.

Also in industry news this week: While RIA M&A deal flow hit record levels in 2024 (both in terms of volume and the speed of completing them), firm valuations saw relatively modest gains In its latest annual regulatory oversight report, FINRA joined the SEC in flagging the potential risks to firm and client data from the use of third-party vendors (..)

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirementplanning, estate and tax planning and mortgage refinancing. They also make up the second biggest client base for financial advisors after baby boomers. trillion annually.

Further, amidst grumbling from some firms, incoming CEO Rick Wurster reiterated a pledge that Schwab (which offers its own direct wealth management services) will not seek to compete for clients with RIAs on its platform, seeing opportunities to pursue prospective clients currently unserved by either group.

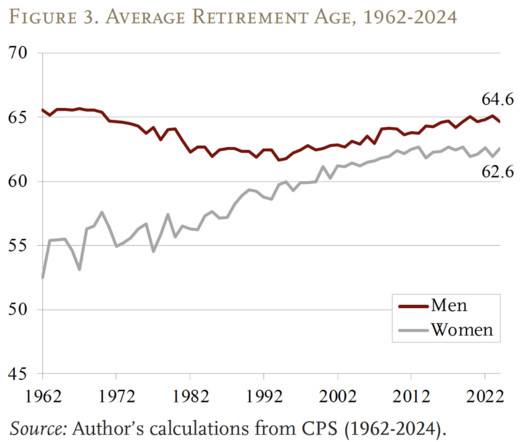

Many financial advisory clients might work for 40 years or more, ideally seeing their income – and capacity to save for retirement – increase over time as they advance in their careers. Still others, including adherents of the Financial Independence Retire Early (FIRE) movement, may hope to retire even sooner.

Which suggests that, amidst ongoing debate over fiduciary-related regulations, an advisor's status as a fiduciary could both lead to greater client trust (both in their individual advisor relationship and perhaps in the financial advice industry as a whole) and, ultimately, higher client retention rates.

(kitces.com) Estate planning Estate plans are a big lift for everyone, including advisers themselves. kindnessfp.com) Why clients need to organize their digital assets for estate planning purposes. riabiz.com) This money manager's ETF business was built on entertaining clients. abnormalreturns.com)

A new WMIQ study on retirementplanning, conducted in collaboration with annuity provider Midland Advisory, found more than 3/4 of potential clients feel it’s important for advisors to be fiduciaries and nearly 2/3 prioritize retirement expertise.

Notably, the survey identified differences in workplace flexibility by role (with client-facing advisors working more days per week in the office) and by experience (with newer firm employees more likely to have more in-office days each week).

(kitces.com) Peter Lazaroff talks with Christine Benz about the most overlooked parts of a retirementplan. riabiz.com) The battle over online estate planning is only heating up. riabiz.com) The battle over online estate planning is only heating up. How to talk to clients about tariffs.

While it may take a while for the adjustments to take place, advisors can still help their clientsplan for the effect of WEP and GPO's repeal by estimating how much the client will be receiving in Social Security benefits once the new law is implemented. will be top of mind for clients affected by the WEP and GPO.

Vestwell conducted the fourth-annual “Retirement Trends Report” in fall 2022 and received responses from almost 1,300 savers, 500 financial advisors and 250 small businesses.

manages about $300 million in client assets. Jacob William Advisory has proactively recruited next-generation advisors as part of its business continuity plan. Dixon-James launched Resilient Wealth Management in 2020 and now manages about $250 million in advisory, brokerage and retirementplan assets.

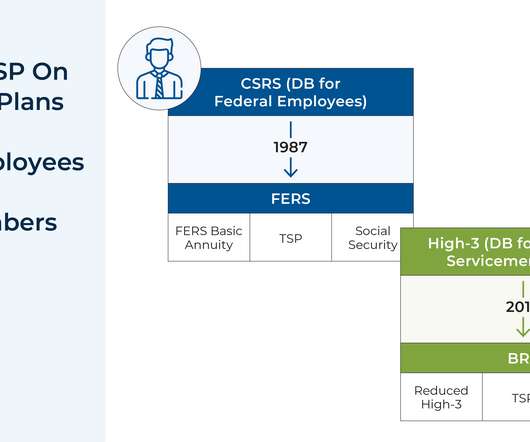

Seasoned financial advisors have likely worked with clients with a wide variety of workplace retirement accounts, which can vary in terms of their investment offerings, fees, and other characteristics. But given that the U.S. But given that the U.S. While many features of the TSP (e.g., While many features of the TSP (e.g.,

Historically, advisors haven't had many avenues to manage clients' 401(k) plan accounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content