This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Prior case law in the Southern District of New York (Morales v. Quintiles Transnational Corp. 2d 369 (S.D. 1998) and Donoghue v.

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. Find your next tax advisor at Harness today.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

Donor-advised funds (DAFs) have emerged as powerful tools that deliver this exact combination, providing immediate tax advantages while offering flexibility to recommend grants to qualified organizations over time. DAFs also introduce welcome simplification at tax time by consolidating multiple charitable activities under a single receipt.

So I would urge planners and individuals pursuing their own retirement plans to think about building in some of those lifetime, uh, giving, uh, aspirations. And also, you know, there are really nice taxplanning mechanisms that people can use to help them achieve, achieve those things as well. Why is figuring out. Definitely.

Consider tax-advantaged options , such as ESOPs, which allow for capital gains tax deferral when proceeds are reinvested, or stock sales that may qualify for preferential long-term capital gains treatment. The most common exit options include mergers and acquisitions, asset sales, stock sales, and employee ownership plans.

If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made. What is a Donor Advised Fund?

This approach typically provides greater benefits to those who have significant assets and high taxable income in retirement. Tax-free withdrawals Five years after the year in which you make a Roth conversion or first open the account youre able to withdraw funds for qualifying events without a penalty.

The IRS implements whats known as the wash-sale rule, which prohibits you from buying a substantially identical security within 30 days before or after the sale of a loss-producing asset. Defer income where possible Strategically timing your income can have a major effect on your tax liability. Available to taxpayers aged 70.5

This article explores the distinctions between K-1 and 1099 reporting, explaining their impact on taxplanning, basis calculations, filing deadlines, and strategies to optimize your after-tax returns from alternative investments.

In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations. From maximizing deductions to managing capital gains, we’ll cover everything you need to know about smart taxplanning.

Estate planning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

What are tax-efficient alternative investment structures? Tax strategies for high-income filers How Harness can help FAQs What are alternative investments? Alternative investments encompass a broad range of assets beyond traditional stocks, bonds, and cash.

Other reasons involve changes in investment strategy, portfolio rebalancing, or a simple desire to exit a specific asset class. Instead, partners (investors) are taxed directly on their share of the fund’s income, gains, losses, and deductions, regardless of whether those amounts are actually distributed.

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. She wants to minimize taxes while aligning her legacy with charitable values. Individual results will vary based on specific financial circumstances.

But you might consider increasing your impact by setting up a structured , long-term philanthropic plan such as an endowment. An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan.

The Tax Cuts and Jobs Act of 2017 eliminated recharacterization, transforming Roth conversions into permanent decisions requiring thorough analysis before execution. Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs.

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. LPs are governed by a partnership agreement that outlines the roles, responsibilities, profit distribution, and other operational details.

Here are five reasons we suggest skipping nondeductible IRA contributions: How non-deductible contributions are taxed Never-ending recordkeeping requirements Capital gains tax rates vs ordinary income State tax rules, inherited IRA issues, and RMDs Other accounts may be better retirement planning vehicles 1. Yes and no.

What Are Qualified Charitable Distributions (QCDs)? For those over 70½, you might already be familiar with Qualified Charitable Distributions (QCDs). For years, QCDs have allowed people to donate directly from their IRAs without paying taxes on those distributions.

Property taxes: These local taxes are based on assessed property value and are generally deductible, though federal limitations may apply to total state and local tax (SALT) deductions. Capital gains tax: Profits from selling property are subject to capital gains tax.

What is a capital gains tax? When you sell an asset like a stock or a home, your gain could be taxable. The tax rate will depend on several factors, such as your holding period, type of asset, and your taxable income for the year. What is a capital gains tax? Single and married filing jointly are the most common.

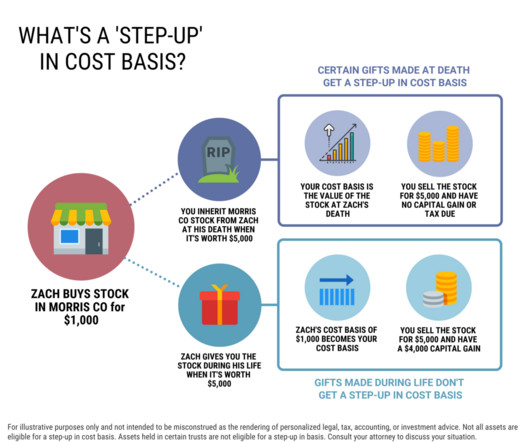

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Heres how stepped up cost basis works on stock and other assets at death. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets.

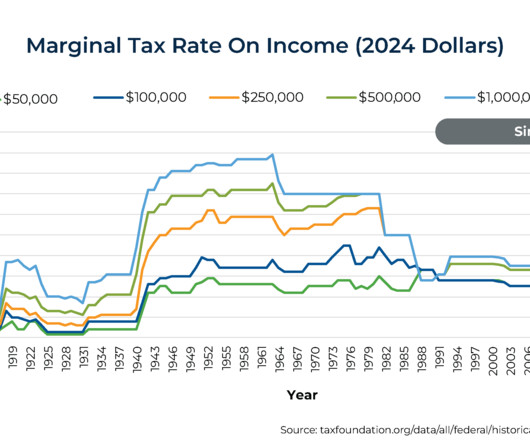

Unless Congress intervenes, the TCJAs sunset will usher in a swathe of tax increases in 2026, with analysts estimating that over $4 trillion worth of tax hikes could take effect. Additionally, there were temporary changes for individual income taxes, such as lower tax rates and a near doubling of the standard deduction.

In this article, well explore all the details of alternative investments, the reasons behind their growth as an investment choice, and how their tax treatment differs from traditional assets. Well also go into some potential strategies to optimize tax efficiency. What Are the Tax Strategies for Alternative Investments?

Know the Distribution Rules Distribution requirements depend on the type of IRA and your relationship to the deceased. Multiple beneficiaries: To avoid defaulting to the oldest beneficiarys distribution schedule, set up separate accounts by Sept. Whether inheriting a Traditional or Roth IRA, understanding the rules is crucial.

The Bible doesnt lay out a detailed blueprint for modern estate planning, and thats okay. These guidelines include: Stewardship: Recognize that all assets belong to God and plan accordingly. Charitable Giving Plan: Develop a strategy for supporting Christian ministries and charities.

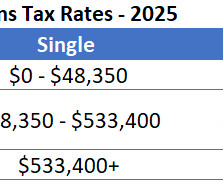

Enjoy tax-free growth and withdrawals. No required minimum distributions (RMDs). Drawbacks: Conversions may trigger taxes. Potential to move into a higher tax bracket. You must hold a Roth IRA for at least 5 years to benefit from its tax-free withdrawals. GET STARTED What are the capital gains tax changes in 2025?

For executives and entrepreneurs holding highly appreciated assets, the need for diversification becomes increasingly important. Selling stock outright, however, can incur a sizable tax billmaking it difficult to balance concentration risk with long-term portfolio preservation.

Asset and Liability Matching. Good financial planning is all about asset and liability matching across time. That means you need to make sure you understand how your income and assets relate to your expenses and liabilities. A financial plan with an asset liability mismatch is likely to fail over time.

Losing a spouse is a difficult time, and navigating the complexities of inherited assets can feel overwhelming. The Single Life Table typically results in higher mandatory distributions. Note that if the deceased account holder had not yet taken their RMD for the year of death, that distribution must still be taken.

Key Takeaways: Net Unrealized Appreciation (NUA) is the difference between the cost basis of employer securities in a retirement plan and their market value at the time of distribution. NUA is not taxed as ordinary income at the time of distribution, which can offer significant tax advantages.

The bucket strategy solves this by dividing your assets based on time horizon: Bucket 1 (0 to 3 years): This is your short-term spending fund. Bucket 3 (10+ years): This is where you keep equities or real estate, assets built for growth. Roth conversion ladder Here’s a tax strategy that many overlook until it’s too late.

Retirement-related behavioral and financial changes raise many taxplanning questions and opportunities. A trusted tax professional can help you implement these and other strategies to help you minimize taxes in retirement, helping your money last longer and you realize your goals.

The second amendment to the revocable trust agreement directed the following distributions: • 2 million dollars to the trustee of the MCC Trust, to be held for Maria’s benefit. The MCC Trust agreement included terms about the distribution of trust assets: 3.2. Administration of Trust Estate for Beneficiary.

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B Lothes July 17, 2025 6 Min Read • Distributions of stock in a grantor retained annuity trust (GRAT) don’t trigger insider trading rules— In Nosirrah Management, LLC v. The court determined that one distribution qualified, while the other didn’t. Handler, Alison E.

Key among them are the options to roll over the account into their own IRA, keep it as an inherited IRA, or consider varying stances based on the decedents Required Minimum Distributions (RMDs). Unlike non-eligible beneficiaries who are limited to a strict ten-year distribution period, EDBs can choose from various withdrawal schedules.

Estate planning is not just for the wealthy; it is essential for anyone who wants to ensure their assets are managed and distributed according to their wishes. A lack of estate planning can lead to significant complications. An effective estate plan does more than simply divide assets.

As a result, there's a common line of thinking that people saving for retirement should avoid pre-tax retirement accounts entirely and contribute (or convert existing pre-taxassets) to Roth instead – regardless of which tax bracket they're in today.

As we begin our countdown to 2024, it is a great time to ensure your year-end taxplan is in place. Taxplanning is a vital component of meeting your overall financial goals. Our team of professionals is here to assist with your financial and taxplanning needs. You can access the webinar recording here.

Further, unlike retirement accounts, assets in a brokerage account can be used for any purpose at any time without early withdrawal penalties. Retiring early is also even more difficult without taxable assets as you’ll need to bridge the gap before penalty-free distributions from 401(k)s or IRAs begin, perhaps to cover medical expenses.

Cost-saving taxplanning can be much more difficult to implement after your company is well-established and has reached the stage where an IPO, merger, or acquisition becomes a likely event. The first three options are pass-through entities, so profits and losses are distributed to the owners who are taxed on them.

For example, if you convert $50,000 and it grows to $100,000 in a Roth IRA over the next several years, that essentially results in $50,000 tax-free dollars. Keeping your funds in a traditional IRA only defers taxation on the full amount until the funds are distributed at some point in the future.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content