This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

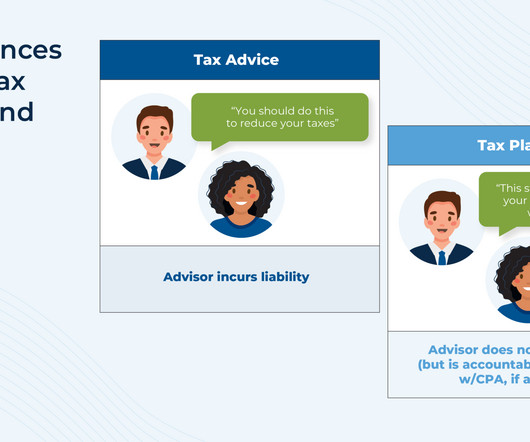

In recent years, financial advisors have increasingly embraced taxplanning as a core element of delivering value to clients. Despite this growing interest in tax conversations, most advisors are still quick to distinguish their services as "taxplanning", not "tax advice" – a distinction largely driven by liability concerns.

Griffin is the owner of GK Wealth Management, an RIA based in Reno, Nevada, that oversees $200 million in assets under management for 450 client households.

As a result, financial advisors should start honing the services Gen X members will likely benefit from the most, including retirement planning, estate and taxplanning and mortgage refinancing. Younger Gen Xers tend to be more akin to millennials, preferring shorter, more frequent digital communication from their advisors.

RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth Jalina Kerr of Charles Schwab shares how the most adaptive firms are expanding beyond portfolio management, into areas like estate and taxplanning.

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B is joining the trend toward combining wealth management and taxplanning by merging with Brookfield, Wis.-based Mergers and partnerships between RIAs and tax firms have moved beyond sharing client referrals to bringing the practices into one firm or relationship.

Technology deductions extend beyond basic communications to encompass computer equipment, software licenses, and various technology subscriptions essential for business operations. Understanding these limitations and planning accordingly can help maximize QBI benefits while maintaining compliance with IRS regulations.

Financial planning can give you the tools, resources, and confidence to conduct your financial life on solid footing. A financial plan looks at your assets and liabilities, short-term and long-term needs, as well as your goals to structure your finances in a way that suits you. TaxPlanning. Want to retire early?

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. Identifying and leveraging these opportunities is a vital part of effective taxplanning.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Gifting Other than transferring assets after death, the other primary way to transfer wealth is to gift portions of your estate during your lifetime.

When you have the resources to make an impact, this type of planning helps you pinpoint what you want to accomplish for your family, community, and society. Steps to Setting Up a Philanthropy Fund Taking the proper steps in the beginning can give your charitable giving plan a solid foundation.

But you might consider increasing your impact by setting up a structured , long-term philanthropic plan such as an endowment. An endowment is a portfolio of assets that is invested to provide support for a cause. Donations to endowment funds are tax-deductible, giving them a place in your overall financial management and taxplan.

Despite removing the recharacterization safety net, the Tax Cuts and Jobs Act left intact the fundamental benefits that make Roth conversions attractive: tax-free growth potential, freedom from required minimum distributions, and tax-free qualified withdrawals.

Property taxes: These local taxes are based on assessed property value and are generally deductible, though federal limitations may apply to total state and local tax (SALT) deductions. Capital gains tax: Profits from selling property are subject to capital gains tax.

We start with several articles on retirement planning: Why considering a client's retirement time horizon and spending flexibility could lead to more accurate (and often higher) safe withdrawal rates than the simpler "4% rule" Four unique risks retirees face when drawing down their assets, from sequence of returns risk to tax risk, and how financial (..)

These guidelines include: Stewardship: Recognize that all assets belong to God and plan accordingly. Fairness: Promote unity by communicating the plan to heirs. Planning for Contingencies: Prepare for unforeseen circumstances, like disability or illness. Generosity: Pass along wisdom before passing along wealth.

Estate planning is not just for the wealthy; it is essential for anyone who wants to ensure their assets are managed and distributed according to their wishes. Whether you own an elaborate portfolio or a single family home, having a comprehensive plan in place can protect your legacy and provide peace of mind for your loved ones.

Going beyond FPA’s existing PlannerSearch tool, the narrowed-down list is meant to help consumers identify a focused subset of the most reputable planners.

Although many investing and wealth-preservation principles apply to anyone – such as developing a taxplan, assessing a portfolio’s risk exposure, and more – there are key risks to be aware of when you have more money and more valuable assets to protect. Being Too Conservative. Not Taking Inventory of Collectibles.

The ‘millionaires’ tax will also ensnare taxpayers who exceed the $1M limit after selling a home, business, stock options, or other types of one-time events. Article is a general communication only and should not be used as the basis for making any type of tax, financial, legal, or investment decision.

What are appropriate checklists for year-end taxplanning? Tax planners often develop checklists to guide taxpayers toward year-end strategies that might help reduce taxes. Certain tax benefits may be available if you can claim an individual as a dependent. Family taxplanning. Financial investments.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

You expect your future tax rate will be higher than it is today Time value of money. All else equal, you’d be better off paying tax next year instead of today. If you have a large pool of pre-taxassets, when RMDs kick in you could have little protection against the highest tax brackets.

Asset management Connecting investors to what matters most, so they can achieve their goals and make confident decisions. That matters because inheritance, of course, translates to investable assets. trillion in investable assets by 2030, which balloons to $70 trillion in investable assets by 2045.* Varied communications.

SmartOffice — SmartOffice , the customer relationship managemen t s olution from Ebix, is a financial planning CRM that helps financial advisors tackle critical tasks like analysis, communication, and client services. . CRM systems make it easier to juggle tasks, opportunities, and communications.

The problem was that I couldn’t give these younger clients the time of day in that setting because they didn’t have enough investable assets yet. Tax and insurance advice was also somewhat constrained. Then we do the financial plan and taxplanning around that—it’s been a lot of fun.

Whether you are contemplating forming an LP or already operate one, gaining clarity on tax matters can optimize your financial outcomes and ensure compliance with state and federal regulations. Identifying and leveraging these opportunities is a vital part of effective taxplanning.

According to a Fidelity study, 45 percent of younger investors are more inclined to consolidate their assets with one advisor as opposed to spreading assets across multiple advisors. Identify what value you bring to clients in each of your target segments and then communicate that value via the right channels.

By exploring these nuances, you can better appreciate the tax advantages and responsibilities that come with running a Co-op. Understanding Co-op Taxes Key Tax Deductions and Credits Taxplanning tips for a Co-op Final Thoughts on Understanding Co-op Taxes Partner with Harness for Expert Tax Support What Is a Cooperative (Co-op)?

Unlike an endowment, taxes really matter. It’s a shift of mindset from the earlier days, when they were building their wealth, and we were more focused on income taxplanning. What we often see is people are too late to think about estate taxes. The remaining assets are then given to charity when the trust ends.

Your risk tolerance will influence your investment strategy and asset allocation. Certified Public Accountant (CPA) CPAs specialize in taxplanning and accounting. While they may not be exclusively wealth managers, their expertise in tax matters can be invaluable in managing your taxes efficiently.

Several of the wealth managers had specialists in-house such as: Chief Philanthropic Advisor, Head of TaxPlanning, Family Legal Counselor, Trust Officer If you can’t hire these specialists, work out an arrangement with a close third-party with this expertise. Wear a suit and present yourself conservatively.

Ultra and very high-net-worth individuals may also have assets valued at more than $5 million and $30 million. Moreover, these high-net-worth values are not calculated on physical assets but on liquid ones, which may be relatively more volatile to manage. Income tax, capital gains tax, property tax, estate tax, state tax, etc.,

presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estate planning and a host of other topics. Since last year’s U.S. Those conditions do not exist today.

This tax benefit is scheduled to sunset at the end of 2026. Taxplanning for 2026 Depending on your situation, income, and goals, your planning options will vary. As with anything in taxplanning, it’s important not to let the tax-tail wag the dog.

Financial planning can give you the tools, resources, and confidence to conduct your financial life on solid footing. A financial plan looks at your assets and liabilities, short-term and long-term needs, as well as your goals to structure your finances in a way that suits you. Overpaying on taxes. TaxPlanning.

Your risk tolerance will influence your investment strategy and asset allocation. Certified Public Accountant (CPA) CPAs specialize in taxplanning and accounting. While they may not be exclusively wealth managers, their expertise in tax matters can be invaluable in managing your taxes efficiently.

Expertise in TaxPlanning & Compliance: A CPA can help you identify tax-saving opportunities and help keep your clients in compliance with tax laws, reducing the risk of costly penalties and fees. This can allow you both to work together to come up with solutions before tax season.

Further, it means selling other diversified assets (or using cash) to fund the put option purchase, essentially furthering the concentration in the stock. Tax-loss harvesting can also create unnecessary turnover in a portfolio and large gaps between the current and target asset mix. Only long-term securities are eligible (e.g.

The goal of diversification is for your portfolio assets to balance each other out by maximizing profit and minimizing risk. You can diversify your portfolio across asset classes, within assets, and also geographically (think both domestic and foreign markets). Asset Allocation. Building Your Strategy.

For others, it’s a “pull” or desire to do more for clients by becoming a true fiduciary—and enhancing service, support, technology, and communications in the process. Better communication. Today clients are looking for a “financial quarterback” that can advise on all aspects of their wealth. A clear win-win!

In case of any doubt or discrepancies, it is vital to communicate with your financial advisor openly. Communication is key in the evaluation of investment performance. Communication is key in the evaluation of investment performance. Transparent communication is paramount in risk management.

Investment advisors can also specialize in specific areas such as retirement planning, taxplanning, or portfolio management. Credit Manager: Credit managers are professionals responsible for overseeing and supervising credit assets within an organization. Excellent communication and interpersonal skills.

Think of your net worth as a summary of your total financial value – your assets minus your liabilities. The average age of stressed millionaires (66) is lower than less-stressed millionaires (67) The number of investable assets between the two groups is equal ($1.75 Well, you might already be one!

Understanding Wealth Management Wealth management is helping high-net-worth individuals and families manage their financial assets and plan for their future financial needs. Wealth managers collaborate with their clients to develop customized strategies for asset allocation, taxplanning, estate planning, and risk management.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content