This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with a recent survey indicating that a majority of advisors are viewing new client acquisition as their primary challenge in the current competitive environment for financial advice (followed by compliance and technology management) and suggests (..)

The study also identified factors that separated firms experiencing the greatest organic growth from others, which include offering a comprehensive suite of services, having a higher 'close' rate with prospects, and, perhaps counterintuitively, a lack of satisfaction with their client experience. Read More.

For many small tax firms, the process of collecting client tax documents can be a time-consuming and a prolonged process. Tax advisors often find themselves sending multiple reminders, following up on incomplete files, and waiting for clients to gather the necessary paperwork. Read more about Kelley Maddoxs success here.

Key Takeaways: Too many tax practices are bogged down in commoditized administrative tasks and compliance work, making it challenging to cross-sell services to expand client relationships. The more a firm can either automate processes or outsource tasks, the more time it’ll have to build deeper client relationships.

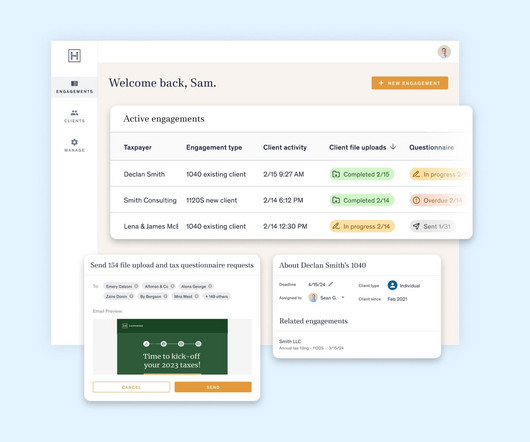

Key Takeaways: CRM system centralizes all client and prospect information, helping tax firms manageclient interactions and replacing manual systems like spreadsheets. A client portal serves as a one-stop shop for client collaboration and managingclient tasks.

Estate and gift tax planning Maximize gift tax exemption: Encourage clients to use the currently higher $13.61 Estate and gift tax planning Maximize gift tax exemption: Encourage clients to use the currently higher $13.61 million (single) / $27.22 million (married) gift tax exemption before it drops in 2026. million (single) / $27.22

CRM stands for Customer Relationship Management and is a technology used to manage your advisory’s relationships and interactions with clients. Whenever CRM is mentioned, it’s usually in reference to a tool that can manage customer relationships across an entire lifecycle. What is CRM?

Most importantly, tax practices are built on strong client relationships and specialized knowledge. In this article, well examine the key considerations of tax practice succession planning, from initial preparation to a strategic exit, and how best to secure your firm’s continued success.

Estate and gift tax planning Maximize gift tax exemption: Encourage clients to use the currently higher $13.61 Estate and gift tax planning Maximize gift tax exemption: Encourage clients to use the currently higher $13.61 million (single) / $27.22 million (married) gift tax exemption before it drops in 2026. million (single) / $27.22

These advisors vary in terms of their areas of expertise and the specific types of financial services they provide, and tailor their advice to their client’s financial situation, needs, and goals. This article discusses the different types of financial advisors you can choose from based on your specific financial needs and goals.

From being able to provide rate estimates to prospective clients to responding to inquiries and even pitching life insurance policies, agents have a knack for understanding the ins and outs of life insurance. Knowing how much protection clients qualify for is a critical part of their job. Management and Leadership Skills.

Most importantly, tax practices are built on strong client relationships and specialized knowledge. In this article, well examine the key considerations of tax practice succession planning, from initial preparation to a strategic exit, and how best to secure your firm’s continued success.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content