This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. HSA accounts can only be used in conjunction with a high-deductible health insurance plan.

Historically, advisors haven't had many avenues to manage clients' 401(k) planaccounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

Historically, advisors haven't had many avenues to manage clients' 401(k) planaccounts, since unlike traditional custodial investment accounts, advisors generally lack discretionary trading authority in employer-sponsored retirementplans.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

30 years ago, when financial plans relied mainly on constant investment return projections derived from straight-line appreciation and time-value of money calculations, financial advisors began acknowledging and accounting for the variable and uncertain nature of investment returns.

often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement. Focus on Your RetirementPlan Rather Than a Magic Number. would be “How do I plan for retirement?“ Social Security is a federal retirementplan originally created under the Social Security Act of 1935.

By distilling hundreds of pieces of information into a single number that purports to show the percentage chance that a portfolio will not be depleted over the course of a client's life, advisors often place special emphasis on this data point when they present a financial plan.

Last year’s considerable losses and market fluctuations underscore the need for clients to assess their retirementplans to ensure it aligns with their objectives, financial situations, timelines, and attitudes toward market volatility. You can help them start the year right by conducting a retirement checkup.

Rather I suggest an investment strategy that incorporates some basic blocking and tackling: A financial plan should be the basis of your strategy. Any investment strategy that does not incorporate your goals, time horizon, and risktolerance is flawed. View all accounts as part of a total portfolio.

Hypothetical simulation assumes $1M was invested on 12/31/2004, 50% in SPY and 50% in AGG, portfolio was never rebalanced, dividends not reinvested, and no other contributions/withdrawals in the account. Hypothetical simulation uses current yields and assumes 60% of the account is invested in SPY and 40% AGG. versus 1.1%

With medical inflation outpacing general inflation, ignoring healthcare in your retirementplan is a risk no one can afford. Factoring in retirement healthcare costs is a smart move. And if you are unsure where to begin, talking to a financial advisor can help you build a more personalized and realistic retirementplan.

As someone saving for retirement , what should you do now? During the financial crisis there were many stories about how our 401(k) accounts had become “201(k)s.” The PBS Frontline special The Retirement Gamble put much of the blame on Wall Street and they are right to an extent, especially as it pertains to the overall market drop.

Saving for retirement is a long-term endeavor. It requires a different perspective on your wealth and income that accounts for your needs in different stages of your life, from the beginning of your working years through your retirement. It’s not about finding the next hottest stock or trying to get rich quickly.

While they do share some similarities, there are enough distinct differences between the two where they can just as easily qualify as completely separate and distinct retirementplans. Though they can’t legally own an account, an IRA can be set up as a custodial account. in a taxable account (assuming a 25% tax rate).

While grappling with various aspects of retirementplanning, it is imperative to acknowledge a critical factor that often does not receive its due attention – longevity risk. Longevity risk refers to the risk that people are living longer lifespans than previous generations.

residents 18+ and subject to account approval. residents 18+ and subject to account approval. Minimum Investment: $2 and up Stability/Risk Level: Low stability / high risk Liquidity Level: Moderate to high Transaction Costs: 0 to 5%, depending on crypto Where to Invest: BlockFi , Crypto.com , Gemini , Coinbase , Robinhood.

Take Advantage of RetirementPlans and Matching Contributions. Most employer retirementplans allow you to save on a tax-deferred basis, meaning that contributions into these types of accounts are not considered in calculating your taxable income. . Compounding interest can be power for Lisa.

The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years. Retirementplanning is not just about reaching a target savings number.

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirementplanning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirementplanning.

The SEP-IRA (AKA Simplified Employee Pension) Expert tip: Understand your risktolerance How to save for retirement in your 20s when you’re just starting out How much should I contribute to my 401(k) in my 20s? How much should you be saving for retirement in your 20s? How do I start putting money away for retirement?

For example, you may hold some of your investments with a robo-advisor while maintaining an account with an investment brokerage firm for self-directed investing. Available accounts: Joint and individual accounts; traditional, Roth , rollover, SEP, and SIMPLE IRAs; Solo 401(k)’s ; trusts and custodial accounts.

So if you’ve got ambition and self discipline, maybe you really can retire at 50! Important Considerations if Retiring at 50 is a Real Goal If you want to retire at 50, there are some important considerations to take into account. Your retirementplan shouldn’t be. Ads by Money.

And how does it compare to the 401k and other retirementplans that exist? With the SIMPLE IRA, you are 100% vested whenever the employer deposits that into your account. Being a self-employed retirementplan , the SIMPLE IRA gives you the discretion of what exactly you want your money invested into. .

Although your savings account might have the same balance ten years from now, that money will not have the same purchasing power that it has today. Begin investing money into employer-sponsored accounts. You may work for a company, where you likely have access to some employer-sponsored investment accounts.

Investing in an Individual RetirementAccount (IRA) is an excellent way to save for retirement. 1] What are Your Investment Goals and RiskTolerance When selecting investments for your IRA, consider your investment goals and risktolerance.

Understanding your current financial picture will help you figure out if you’re ready to retire or if adjustments are necessary to secure your future. Review Your Retirement Savings Start by checking your retirement savings accounts, such as 401(k)s, IRAs, and pension plans.

Although your savings account might have the same balance ten years from now, that money will not have the same purchasing power that it has today. It depends on how much you make, when you want to retire, and how much you want in your accounts by then. However, your savings are diminished each day by the powers of inflation.

To rebalance your portfolio, you’ll buy and sell certain investments to realign to your accounts with your desired asset allocation. This is critical because without rebalancing, you may be taking on more risk than necessary to meet your goals. Finally, when rebalancing your 401(k), don’t forget about your other accounts!

The 401(k) plan is the largest asset many investors own accounting for 36.2% Regularly checking your 401(k) account can help you stay on top of your investments, and make sure that your money is working for you in the best way possible. What if You Have Multiple 401k Accounts? Census Bureau. What is a 401k?

Invest in the Stock Market Suggested Allocation: 40% to 50% Risk Level: Varies Investing Goal: Long-term growth The stock market is where most of us save for retirement already, mostly through the use of tax-advantaged retirementplans, like a 401(k), SEP IRA, or Solo 401(k). The best part?

This data can serve as a baseline for tailoring your retirementplan, taking into account factors such as inflation, your current age, and your desired retirement age. Some retirement experts recommend the 80% rule as a practical guideline to estimate your retirement needs. of overall expenses.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

Here are a few examples of how they can help with your financial planning: Create a Comprehensive Financial Plan: A fiduciary and fee-only advisor can work with you to create a comprehensive financial plan that takes into account your goals, assets, and risktolerance.

Are you good with numbers, accounting, and financial planning? If yes, then DIY financial planning might be a good option for you. On the other hand, if you tend to struggle with budgeting or find financial planning overwhelming, then professional money management could be a better solution.

The reality for those with various employers is that untracked retirement savings might lead to missed financial growth opportunities and instability. Diligent oversight and management of these retirementaccounts is essential for anyone aiming to build a solid financial foundation for a comfortable and secure retirement.

I also owned the name for a couple of more risktolerant clients. For a ten year run ending Jan 1, 2019 though it compounded at over 6% annually plus that dividend yield on top and a very low beta. To me, that was a great mix of attributes. At some point along the way I lost faith in China from the top down and sold it.

Many people invest in their company-sponsored 401(k)s but only sometimes take the time to review the investments within the account. Rebalancing involves adjusting the mix of assets in your 401(k) portfolio to maintain a desired level of risk and return. This may lead to a higher or lower risk profile than initially intended.

When we are busy working to earn a living and spending time with our family, first thing needs to think about is RetirementPlanning. Generally, people think about Retirementplanning after retirement. To plan for retired life important thing is financial plan.

Your financial goals and risktolerance are the roadmap for your entire wealth management strategy, shaping your decisions and the services you require. Long-term goals typically encompass retirementplanning, wealth preservation and estate planning.

Overindulgence in information can lead to poor decisions, and excessive monitoring of your retirementaccount balance can result in stress. Checking your retirementaccount balance too often can have a psychological impact on you. When should you check your retirementaccount balance?

Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. For example, you may invest in tax-advantaged accounts, such as a traditional IRA, because it will offer the most tax benefits.

Of course, one of the most important aspects of retirementplanning is managing retirement taxes. Taxes can significantly impact the amount of money you’ll have for retirement. For example, you may invest in tax-advantaged accounts, such as a traditional IRA, because it will offer the most tax benefits.

For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts. Diversification can help you secure a steady income stream during retirement.

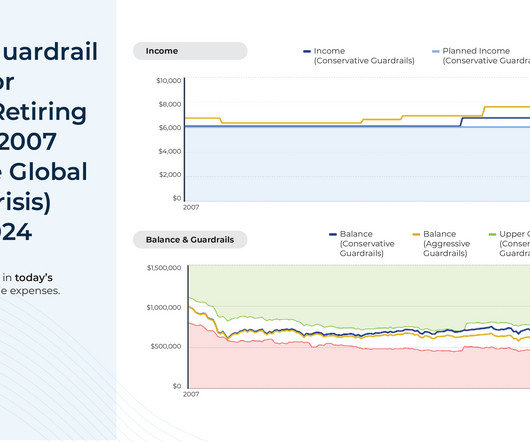

For people nearing retirement, these challenges can be even more daunting. A market downturn at the start of retirement, hitting portfolio values when retirees begin to take account withdrawals, can be unsettling, even for seasoned investors.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content