This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In fact, since the early 1980s, there has been a greater than 5 percent drawdown in the S&P 500 Index every year but two (1995 and 2017)! 8 Assetallocation is an approach to help manage investment risk but it does not guarantee against investment loss.

EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks achen Thu, 06/01/2017 - 02:47 Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another.

Thu, 06/01/2017 - 02:47. Assetallocation—at least for us—is an exercise in nuance. We move slowly and carefully when it comes to shifting our portfolios away from one asset class or region and toward another. EUROPEAN RE-ENTRY: Why We Are Shifting Portfolios Toward European Stocks.

Throughout 2017, our meetings and conversations with clients very frequently focused on the topic of risk. While February’s volatility did not materially change our assetallocation views, it reinforced to us the importance of a comprehensive discussion about how we think about risk and how we manage it. Fri, 03/30/2018 - 11:57.

In their updated “ Summary of Economic Projections ,” they revised their estimates of core inflation for 2023 down from 3.7% Markets were off to the races after the Fed released its statement and economic projections. The average return over rolling five-year periods from 1923 through 2017 is about 11% (before inflation).

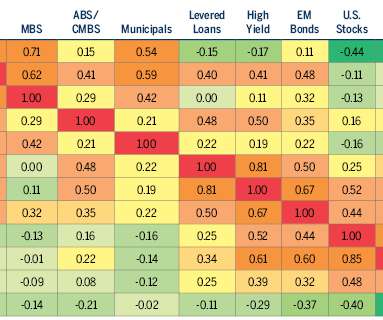

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

As we stated in “Confronting the Unknown,” our 2018 assetallocation publication, standard deviation is “a helpful shortcut for thinking about risk, but it is not a fully effective proxy.” The “shoestring curve” below depicts these risks for a hypothetical portfolio, assuming various assetallocation targets.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy.

In this article, our head of assetallocation discusses how we are managing trade risk, while still embracing global growth opportunities in our portfolios. After an unnaturally serene 2017, volatility roared back into equity markets this year, fueled by worries over interest rates, inflation, tariffs and data privacy.

From an economic perspective, growth in the U.S. Cycles have yet to be eradicated from the economic landscape. equity market’s gain since early 2017 has been concentrated in a relatively small number of sectors and specific stocks. Just to be clear, this is not a sudden or abrupt shift in our thinking. In the U.S.,

From an economic perspective, growth in the U.S. Cycles have yet to be eradicated from the economic landscape. equity market’s gain since early 2017 has been concentrated in a relatively small number of sectors and specific stocks. Just to be clear, this is not a sudden or abrupt shift in our thinking. Incremental Equity Risks.

That’s not suggesting another 2008 is coming, but rather highlights how fast the economic environment can change. Along with the statement, the Committee updated the Summary of Economic Projections (SEP), which is arguably more important than the brief monetary policy statement.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

Further, 2017 overall was extraordinary for its lack of market volatility; the S&P 500 Index rose steadily throughout the year without so much as a 3% pullback—a first in the Index’s long history. For most of 2017, the VIX was exceptionally depressed, signaling that investors expected very little volatility in prices.

ESG and the Stock-Picker’s Dilemma achen Fri, 09/22/2017 - 12:58 One of the greatest challenges that public equities investors face to integrating environmental, social, and governance (ESG) data into their decision making is the lack of proof that real – not hypothetical – investment strategies can use ESG factors to enhance performance.

Fri, 09/22/2017 - 12:58. While these efforts are valuable – they may eventually lead to well-defined ESG factors that resonate with economic principles – it is easy to forget that they cannot prove whether "ESG investing" can be a source of market-independent returns, or alpha. ESG and the Stock-Picker’s Dilemma. References.

Later in the year, markets became anxious about other topics, such as a potential economic slowdown, a new level of dysfunction in Washington (including unusual executive challenges to the Fed's independence and an extended partial government shutdown), and escalating trade disputes between the U.S. equity exposure. and Canada.

There never was a more docile and boring year than 2017. Our article that we linked to above followed the least volatile year in the history of the stock market. Read that sentence again if you must but for some context just let it sink in. Not one single month was down and there was zero volatility. Then… all hell broke loose in 2018.

Multiple Risks Stock prices, the skeptics say, have not reflected the reality of rising economic and political risks. While current economic conditions in the U.S. On one level, this approach sounds simple: Own multiple asset classes or securities so that some perform favorably, while others may be under pressure.

Stock prices, the skeptics say, have not reflected the reality of rising economic and political risks. While current economic conditions in the U.S. Deficit spending, resulting in part from the late 2017 tax reform legislation, is adding to the national debt at a rapid pace that will only worsen as interest rates climb.

Investment Perspectives - The Great Debate achen Wed, 06/21/2017 - 12:35 Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. In short, every situation is different.

Wed, 06/21/2017 - 12:35. Aside from some current political and economic topics that dominate the financial media, the most widely debated investment issue today involves the merits of passive investing, or indexing. Investment Perspectives - The Great Debate. In short, every situation is different.

Bachelor’s in economics and a BS in computer science from Wellesley in Boston and then an MBA from Harvard Business School. So it was Pascal then c plus plus, and then I took an economics class and that’s when the lights went off because it was a very mathematical field in many ways, but also with a link to the Rio economy.

We still like Energy this year and that is especially so with it being one of the most beaten down economic sectors from 2023. If you are comfortable with swings of Bitcoin at $19k in 2017, $4k in 2018, $11k in 2019, $5k in 2020, $58k in 2021, $37k in 2022, $21k in 2023, and now $66k today…by all means hold it!

In that trade on a monthly basis, when you run that full strength, it gives the dynamics of something like the XIV, which rose 600% in 2017, right? And so the institutional space, or most asset selectors, assetallocators are gonna look for managers that are trying to add value. Now my observation was twofold.

But I would add, we had just gone public at the time, 2017. So that was in 2017, we went public on Euronext Paris. RITHOLTZ: (LAUGHTER) CHABRAN: And find a reason why they would allocate there. So I think we’ve now entered a period where we have to swallow this whole mispriced, over-levered assets out there.

Outlook for 2017 | Balance in an Uncertain Time achen Fri, 02/03/2017 - 14:19 With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

Outlook for 2017 | Balance in an Uncertain Time. Fri, 02/03/2017 - 14:19. With that said, we present this discussion of our assetallocation approach and our current portfolio stance as we begin the year. Provide our assetallocation perspective as it stands at the beginning of 2017—also based on a longer-term view.

And it’s funny ’cause that was a pandemic purchase, a very inexpensive 2017 Panama four s, which everybody walked away. You get a BA in economics and poli sci from the University of Delaware. He wasn’t tactical assetallocator. So literally I made a left, right into them. Well, not in college, no.

I know you like to discuss there are different phases of the, of the, both the market and the economic cycle. I mean, we had a global pandemic, a complete shutdown of global economic activity. Think about what, how we were, we were geared in 2017, 2018, 1920. 00:52:12 [Speaker Changed] Exactly.

There’s very few, I would argue probably no consistent predictors of, of any sort of economic or market cyclicality. Most clients, whether they’re individuals or institutions, have some sort of benchmark, a policy portfolio, some strategic assetallocation that they start with. It’s a bit of a mouthful.

Neil Dutta has been doing economic analysis and research from a market-based perspective for over 20 years. I found this to be just an absolutely fascinating discussion about how to best contextualize the world of economic data around you, in a way that’s useful for you as an investor. With no further ado, RenMac’s Neil Dutta.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content