This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

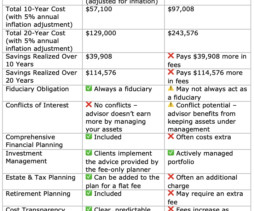

How much to charge for financialadvice is rarely a decision made lightly. Others may align with broader industry trends, like transitioning to fee-only structures to buffer against market volatility. Still others may choose a hybrid model, combining AUM fees with additional charges for other services like tax planning.

The two most common pricing models are fee-onlyfinancial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management). While AUM advisors may seem appealing, they often come with high lifetime fees and potential conflicts of interest.

Hybrid firms can switch between their status as a registered investment advisor and brokerage, which can be problematic for individuals seeking unbiased financialadvice. Benefits of working with an independent fiduciary advisor Independence is important when seeking financialadvice.

Here are five budget-draining mistakes financial advisors often make—and how to avoid them: Overly Broad Keywords Bidding on general terms like “financial help” or “financialadvice” may drive clicks, but not conversions. These keywords attract curious browsers, not committed clients. This improves relevance and control.

riabiz.com) Taxes How pre-tax retirement contributions provide flexibility down the road. kitces.com) Tax strategies if the TCJA expires in 2026. wealthmanagement.com) Advisers 7 more lessons from building an fee-only RIA from scratch.

Enjoy the current installment of “Weekend Reading For Financial Planners” – this week’s edition kicks off with the news that several states are considering a series of tax hikes targeting higher-income and ultra-high-net-worth residents after similar proposals failed to pass at the Federal level.

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that the SEC this week fined 4 RIAs for violations of its marketing rule related to their claims that they offered 'conflict-free' financialadvice.

In November 2022, proponents of the Massachusetts ‘millionaires’ tax (question 1) won their bid to nearly double the income tax rate on individuals with taxable income over $1M a year. As proposed, the new legislation would increase these tax rates to 9% and perhaps even 16% , respectively, starting in 2023.

The post How Conflicts of Interest Shape FinancialAdvice: A Conversation with Mike Garry and Amy Patterson appeared first on Yardley Wealth Management, LLC. Together, they discuss how conflicts influence decisions around Social Security, mortgages, and real estate, while highlighting the importance of working with fee-only advisors.

An RIA firm’s financial advisors must follow the fiduciary standard which is believed to be the highest standard of care in the industry. Fee-only advisor – This is an advisor that does not charge commissions and hence is believed to be more aligned with the client’s best interests.

Consult with a professional financial advisor and receive expert guidance on how to achieve your financial goals like building a significant retirement corpus, lowering your taxes, or creating an investment strategy suited to your needs. . What are the disadvantages of hiring one financial advisor?

When I started Vincere Wealth as a fee-only practice, the vision was to become the go-to place for Millennials who need help with their money. Tax and insurance advice was also somewhat constrained. Then we do the financial plan and tax planning around that—it’s been a lot of fun.

Knowing the types of financial advisors and their compensation models can empower you to select a professional whose approach aligns seamlessly with your financial goals, risk tolerance, and overall budget. Below are the different types of financial advisors you can choose from based on their fee model: 1.

That’s why we typically prefer passive investing , with a balance of low portfolio expenses, minimal trading costs and tax efficiency. The internet is drowning in financialadvice, both good and bad. The post 10 Money Lessons I’ve Learned as a Financial Planner appeared first on Your Richest Life.

Investing in financial guidance is an investment in your future. The right advisor can help manage your wealth, plan for retirement, navigate tax implications, and more. Here’s a deep dive into the average fees of financial advisors, in 2023. Fee-based : This structure is a blend of fees and commissions.

A financial advisor’s service is equally significant when assessing their value proposition. A reputable financial advisor should provide a comprehensive range of services, including budgeting, debt management, insurance optimization, tax planning, retirement planning, estate planning, and investment management.

The simplest definition of the role of a financial advisor would of that of a person who helps individuals, families, and organizations make decisions related to their investments, taxes, insurance planning, retirement planning, estate planning, and money management. Accounting & Tax Planning Firms. Banks & NBFCs.

I have a newsletter in which I talk about financial advisor lead generation topics which is best described as “fun and irreverent.” I am an irreverent and fun marketing consultant for financial advisors. Why is the fiduciary standard important in financialadvice? What is a conflict of interest in financialadvice?

Money books for financial literacy. You’re not limited to dry explanations about portfolio allocations and tax strategies. Mary Beth Storjohann, CFP®, is a speaker and writer who cuts through the fluff and gives clear, concise financialadvice. . There are plenty of fun, interesting books that will meet you at your level.

Is it better to have a financial advisor or do it yourself? Do you need a financial advisor if you don’t have a lot of money? What types of financial advisors should you avoid? Article related to financialadvice Do you need a financial advisor? When should you get a financial advisor?

Is it better to have a financial advisor or do it yourself? Do you need a financial advisor if you don’t have a lot of money? What types of financial advisors should you avoid? Article related to financialadvice Do you need a financial advisor? When should you get a financial advisor?

What research did you do, and what were the signs that it would be a good target market for a financial advisor? But I’ve found relatively few who have structured themselves tax-efficiently. In a relatively short amount of time, Colton has become “the person” for tattoo artists looking for financialadvice.

This interview with Cody Garrett, CFP, of Measure Twice Financial was mind-blowing. It’s so clear to me what the future of financialadvice is – what it should be – and what it will be. I am an irreverent and fun marketing consultant for financial advisors. What is an advice-onlyfinancial planner?

An hourly financial advisor is someone who provides financial advisor for a set hourly rate. These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, tax planning, and other wealth-related topics. Hourly financial advisors are not common. Jon Luskin.

If eligible, you may be able to exclude up to 100% of the gain from federal taxes when you sell your shares through the capital gains tax exclusion. The potential tax savings simply cannot be understated. Using IRS Section 1202, taxpayers can sell stock potentially free of federal capital gains taxes if the requirements are met.

There are really only two key ingredients for this: Diversification across asset classes AND geographies Time in the market, NOT timing the market There are special tools at the disposal of your investment advisor, such as direct indexing strategies that utilize tax loss harvesting to defray some tax costs of gaining more geographic diversification.

We of course can continue to negotiate around the fringes and help mitigate risk and optimize the transaction to fit a more ideal tax structure. HAMBURGER: And then they don’t look at the tax structure, right? And this seems to be an agreement to — RITHOLTZ: Restrict competition in the space of providing financialadvice.

They go crazy and paint it with BS statements like: Tax-free guaranteed income Can’t lose money asset Upside potential with downside protection Privatized banking Be your own bank Remember that there is a floor to the crediting rate, but that doesn’t mean you can’t lose money. Here’s why that stinks.

Feeonly advisors can now purchase annuities for their clients without having to be licensed agents. And if you want to join the right for higher ethics in financialadvice, join the Transparent Advisor Movement. Scott Salaske is the founder and CEO of Firstmetric , a flat feefinancial advisor firm in Troy, Michigan.

I hope you’ll at least join my newsletter about financial advisor lead generation. Certified Financial Planner Board of Standards, Inc. Return of organization exempt from income tax [Form 990]. Scott Salaske is the founder and CEO of Firstmetric , a flat feefinancial advisor firm in Troy, Michigan. www.cfp.net.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content