This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B I think the combination of those two things makes people like me say, ‘Hey, instead of going down this big acquisition route, and because I don’t want to work at a big firm with a 1% or 2% stake, the only way to go is to do it on your own and start from scratch,’” he said.

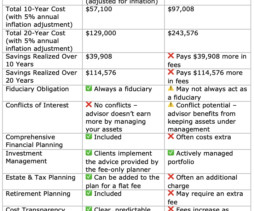

The two most common pricing models are fee-only financial planners (flat-fee or fixed-fee advisors) and AUM-based financial advisors (who charge a percentage of assets under management). While AUM advisors may seem appealing, they often come with high lifetime fees and potential conflicts of interest.

Most fiduciaries don’t sell products: Most fiduciary advisors are only paid by a percentage of assets they manage for clients. This AUM based fee structure is common among fee-only advisors who are almost always full-time fiduciaries. NAPFA advisors are all fee-only financial advisors.

It involves a lot more, such as: Defining your financial goals Understanding your risk appetite Figuring out timelines for each goal Picking the right investment and savings options Managing and tracking your investments Rebalancing your investment portfolio periodically Filing taxes and knowing how your investments are taxed Whew!

And I think you will also, if you are at all curious about estateplanning or investing or personal finance, this is not the usual discussion and I think it’s very worthwhile for you to hear this and share it with friends and family. And I, I found it to be an absolutely fascinating conversation. Right, right.

They want answers to queries like: “Top fee-only advisors for doctors in NYC” “Best financial planners for retirement in Seattle” “Who can help with estateplanning near me?” For example, your “Retirement Planning” page could link to “Social Security Basics” or “Tax Strategies for Retirement.”

riabiz.com) Taxes How pre-tax retirement contributions provide flexibility down the road. kitces.com) Tax strategies if the TCJA expires in 2026. flowfp.com) Don't let the potential for estate law changes be an excuse to not do estateplanning.

Depending on the nature of the windfall, planning opportunities and considerations will vary. For example, the tax laws and distribution terms for an inheritance is quite different to the tax and liquidity considerations during an IPO. In their situation, it meant they could sell all their shares tax free.

Bear in mind that IRA accounts do have income restrictions so it is important to work with your financial advisor or tax preparer to determine if you are eligible to contribute in 2022. Assuming you are eligible, these accounts can be quite tax advantageous for your overall financial situation. 529 College Savings Plans.

Retirement Planning, Income Taxes. She lists much of the basics in her article, including Contribution Limits, Tax Benefits, as well as how to open a SEP IRA and the deadlines for “S” Corps (9/15) and “C” Corps (10/15). Only employer contributions are permitted. appeared first on Yardley Wealth Management, LLC.

Consult with a professional financial advisor and receive expert guidance on how to achieve your financial goals like building a significant retirement corpus, lowering your taxes, or creating an investment strategy suited to your needs. . If you do possess a large estate and portfolio, you can consider hiring multiple financial advisors.

That’s why we typically prefer passive investing , with a balance of low portfolio expenses, minimal trading costs and tax efficiency. While it helps to have a long-term plan that you’re working toward, know that ups and downs are inevitable. Money lesson #8: Estateplanning is important, and nobody really wants to do it.

That will likely be the case this year, too, so if you’re planning on shopping any holiday sales, start looking earlier in November. Get Organized Open enrollment, tax prep and end-of-the-year deadlines can be overwhelming, but they don’t have to be if you get an early start. Check these tasks off your list by Dec.

And ultimately, how to invest a windfall will depend on a number of factors, including your risk tolerance, time horizon, and spending plans. And that’s before even considering taxes or market volatility! Depending on your goals and personal financial situation, there may be many more planning opportunities to consider.

And ultimately, how to invest a windfall will depend on a number of factors, including your risk tolerance, time horizon, and spending plans. And that’s before even considering taxes or market volatility! Depending on your goals and personal financial situation, there may be many more planning opportunities to consider.

.” I’ve heard iterations of this: I’m a CPA and financial advisor, and my best tax return client just hired someone else to do their retirement planning. I’m a CPA and financial advisor, and my best AUM client just hired someone else to do their tax return. I’m a Social Security expert.

A reputable financial advisor should provide a comprehensive range of services, including budgeting, debt management, insurance optimization, taxplanning, retirement planning, estateplanning, and investment management. This would cost you a lot less than paying a percentage of your entire portfolio.

The simplest definition of the role of a financial advisor would of that of a person who helps individuals, families, and organizations make decisions related to their investments, taxes, insurance planning, retirement planning, estateplanning, and money management. Accounting & TaxPlanning Firms.

At the end of our conversation, the reporter asked if we were experiencing an uptick in use of planning software during the current times of crisis. The beauty of creating a plan is that it can help get our clients through the ups and downs of the market – even those caused by a global pandemic. YEP E-Newsletter: [link].

The right advisor can help manage your wealth, plan for retirement, navigate tax implications, and more. Here’s a deep dive into the average fees of financial advisors, in 2023. Fee-based : This structure is a blend of fees and commissions. What Is the Difference Between a Fee-Only and a Fee-Based Advisor?

Here’s an example of a financial plan to ensure you are on track. You’re looking for tax help Tax help should not be confused with financial advisory help. A Certified Public Accountant (CPA) is best equipped to support all your tax needs. They focus on investing, estateplanning, and other aspects of wealth.

Here’s an example of a financial plan to ensure you are on track. You’re looking for tax help Tax help should not be confused with financial advisory help. A Certified Public Accountant (CPA) is best equipped to support all your tax needs. They focus on investing, estateplanning, and other aspects of wealth.

These services often include recommendations on investments, financial planning, retirement, Social Security, Medicare, taxplanning, and other wealth-related topics. RICK FERRI, CFA: What’s more tax efficient? An hourly financial advisor is someone who provides financial advisor for a set hourly rate. Jon Luskin.

Plan for taxes: Estate and inheritance taxes can significantly reduce the value of your assets. It’s essential to work with a financial advisor or estateplanning attorney to develop strategies to minimize tax liabilities and ensure that your beneficiaries receive the maximum benefit from your estate.

They go crazy and paint it with BS statements like: Tax-free guaranteed income Can’t lose money asset Upside potential with downside protection Privatized banking Be your own bank Remember that there is a floor to the crediting rate, but that doesn’t mean you can’t lose money. Here’s why that stinks.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content