This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Handler is a partner in the Trusts and Estates Practice Group of Kirkland & Ellis LLP.

Accumulation-phase planning software won't cut it for solving your clients' complex retirement income puzzles, but there are dedicated applications that can.

While many people approach their financial planning with careful strategy, its easy to overlook the same level of intention when it comes to charitable giving. Lets explore several potentially effective financial planning tools that may help you maximize your impact and meet your philanthropic goals. government.

Act regarding individual retirement accounts, including changing when the first required minimum distribution can be made from the account, new rules for inhe The panel of experts will discuss and answer questions about the changes made by SECURE 2.0

Also in industry news this week: A recent survey indicates that younger "DIY" investors are more likely to be interested in working with a human advisor than their older counterparts, suggesting an opportunity for advisors to tap into this demographic (perhaps by setting minimum planning fees that ensure these clients can be served profitably today (..)

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

Saving for retirement is a major undertaking for most of us. Health savings accounts (HSA) provide another vehicle to save for retirement. Many of you have the option to enroll in high-deductible insurance plans that allow the use of a health savings account via your employer. The rising cost of healthcare in retirement .

Financial advisors have a wide range of strategies at their disposal to create financial plans for their clients. And when it comes to retirementplanning, one popular technique is the use of ‘guardrails’, which set an initial monthly withdrawal rate that can be later adjusted as the size of the client’s portfolio changes.

From a financial planning perspective, the seeming implication of a likely rise in future tax rates would be that, given a choice between being taxed on income today or deferring that tax to the future, it makes more sense to be taxed today when taxes are lower than they'll be in the future.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. Start planning early. And the best way to do that?

We’ve covered a lot of ground with regard to how various tax laws impact your retirementplans: pensions, IRAs, 403(b) and 401(k) plans. But we’ve primarily focused on the US income tax laws (the IRS) affect your plans – and there are many nuances that you need to take into account with regard to state tax laws.

When you are preparing for retirement, you should keep in mind both financial strategies and what tax benefits you may gain. Older citizens can get helpful guidance from the Income Tax Department’s special brochure for retirement taxation matters. Key Tax Advantages for Retirees 1.

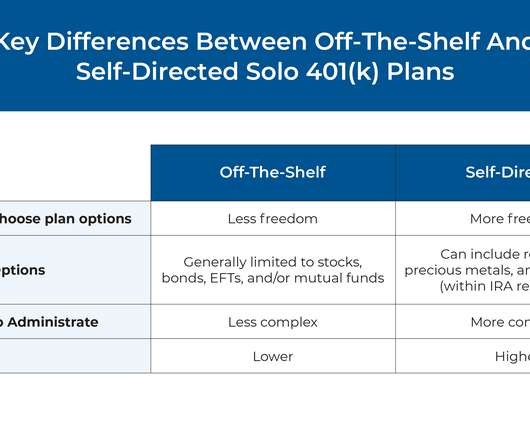

Among the several different types of retirementplans that are available to self-employed workers, solo 401(k) plans can offer the most flexibility and the ability to contribute the highest amount of tax-advantaged savings.

Which means that financial advisors can play an important role in adoption planning – helping clients strategically plan for the costs involved in the process, including accessing tax credits that can significantly defray these expenses. At the same time, adoption can be expensive, with costs that can add up to $70,000 or more.

Traditionally, the challenge in using a 529 plan to save for higher education expenses has been figuring out how much to save to cover the beneficiary's college costs without overshooting and saving more in the 529 plan than is actually needed. The Secure 2.0

Imagine yourself on your last ride home from work on the day you retire. It probably depends on whether you have a strong plan in place for income during your retirement years. Having a retirementplanning checklist can help make this final commute the time of reflection and joy it should be.

Recall last week , we were discussing thinking about the impact of retiring Baby Boomers on the equity markets and of rising rates on housing. The demographic question touches on a big issue: $6 trillion dollars in 650,000 (401k) retirementplans held by 10s of millions of Americans.

Retirementplanning is a journey that generally takes decades to complete and most of us start out along the do-it-yourself path. More than likely, your first step was to enroll in an employer-provided plan such as a 401(k) or setting up an individual retirement account, also known as an IRA.

The other competitors in this year’s demos included Addepar , Altrata , BILL , Encorestate Plans , GReminders , MileMarker , Mili AI , Wealthfeed , Zeplyn and Zocks. There is something to be said for owning your own distribution channel,” he said. s Mili AI won.

We also touched on questions from our audience about holding stocks in your emergency fund, the best way to pay for home renovations, how teachers should factor pensions into their retirementplans and some of my favorite fiction book series.

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations.

When you have the bulk of your financial assets in retirementplans, you might accidentally expose yourself to some risks that you haven’t thought about… since retirementplan assets are much more likely to be impacted by changes to legislation – as we have seen in the past. No related posts.

In case you don’t know what a 72t distribution is, this is shorthand for the Internal Revenue Code Section 72 part t (or IRC §72(t) for short), and the most popular provision of this code section is known as a Series of Substantially Equal Periodic Payments – SOSEPP is the acronym. Enough about the code section already.

understand the value of qualified charitable distributions (QCD). Not only does this money count toward your required minimum distribution (RMD), but the donation is made tax-free, and the funds dont count toward your total taxable income. Note: This only applies to U.S.-based

As December unfolds, it’s easy to overlook year-end tax planning amid the holiday hustle. Maximize Your Retirement Contributions: Enhancing your retirement savings not only secures your future but also offers immediate tax benefits. However, dedicating a few moments now can lead to significant savings come tax season.

Jeff is the Owner and Founder of Cypress Financial Planning, an independent RIA based in Haddon Heights, New Jersey, that oversees $275 million in assets under management for 380 client households. My guest on today's podcast is Jeff Jones.

Each discussed how providing a more holistic approach to distribution-phase planning in their practices can amp up organic growth for advisory firms. I cannot say enough about how well received this last session was by advisors, several of whom came up later to say thanks.

is significant legislation signed into law on December 20, 2022, and is expected to have several impacts on retirement income planning. It contains several provisions designed to improve Americans' retirement security, including later required minimum distributions (RMDs), 529-to-Roth rollovers, and other tax planning opportunities.

From there, we have several articles on retirementplanning: The latest rules for 2023 Required Minimum Distributions from inherited retirement accounts. Why relying on Treasury Inflation-Protected Securities (TIPS) to support the bulk of retirement income needs could be risky.

Whether they are on the cusp of retirement or living as a retiree, this is an impactful time of transition. Navigating the Retirement Transition with “Switches” Because the transition to retirement is dynamic and requires financial, lifestyle, and social choices, clients need a full understanding of their “switches” or options.

Did you know that there is a specific order for distributions from your Roth IRA? The Internal Revenue Service has set up a group of rules to determine the order of money, by source, as it is distributed from your account. This holds for any distribution from a Roth IRA account.

In 1974, Congress passed the Employee Retirement Income Security Act (ERISA) that, among many other provisions, provided for the implementation of the Individual Retirement Arrangement. The Education IRA was also introduced, with features similar to the Roth IRA (non-deductible but tax-free upon qualified distribution).

”, a series of measures that will have significant impacts on the world of retirementplanning. A review of financial planning actions, from tax-loss harvesting to charitable giving, that have a December 31 deadline.

Rowe Price has acquired Retiree Income, the parent company of popular retirement income planning software SSAnalyzer and Income Solver, to put its resources behind developing and distributing the company’s planning tools (albeit perhaps more to its retail and employee retirementplan clients than to advisors?).

Unlike most types of retirementplans, the SEP IRA is funded by the employer. A SEP IRA (Simplified Employee Pension Individual Retirement Account) is a type of retirementplan specifically designed for self-employed individuals and small business owners. Again, all eligible employees must be covered by the plan.

Proactive year-end tax planning can lead to significant savings and set you up for financial success in the new year. Checklist: Year-end Tax Planning Strategies Review the following tax strategies with your tax advisor and/or financial advisor before the end of the year. GET STARTED 1. For those over 50, the limit is $8,000.

This month's edition kicks off with the news that held-away asset management platform Pontera has raised $60 million in venture capital funding as advisors increasingly seek to directly manage clients' 401(k) and other outside assets – although an ongoing investigation by Washington state regulators over whether advisors' use of Pontera violates (..)

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

Congress is once again poised to make sweeping changes to the retirement and tax rules in the last two weeks of the year. retirement changes. retirement changes. Raise the required minimum distribution age. 529 plan to Roth IRA rollovers. The Secure Act 2.0 is expected to become law later this week.

Act have affected millions of Americans inheriting or leaving behind a retirement account. While required minimum distributions (RMDs) for the account owner are delayed, there is now a 10-year window for many people who inherit these accounts to take their distributions. The SECURE Act and SECURE 2.0

From there, we have several articles on investment planning: While I Bonds have received significant attention during the past year, TIPS could be an attractive alternative for many client situations. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S., Also in industry news this week: Most businesses that operate in the U.S.,

If you think retirementplanning moves stop at retirement, think again. Although it won’t make sense in every situation, retirement can be a unique opportunity for Roth conversions for some investors. For high earners, converting an IRA to a Roth IRA while you’re still working could be the worst time of all.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content