This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

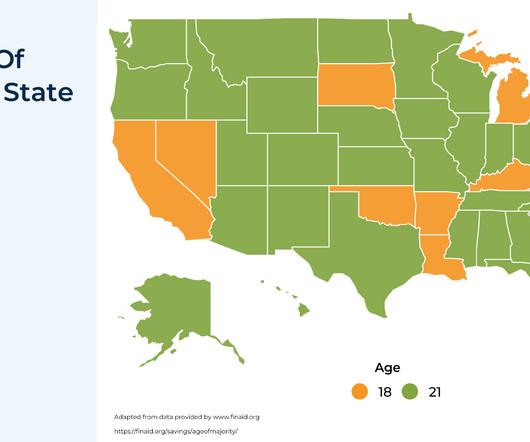

To achieve this, financial support may start at a very young age, allowing for a longer growth horizon and, in many cases, serving tax and estateplanning purposes. However, once a child reaches the age of majority, they may not always be in a position to manage assets responsibly.

Related: Planning for Older Clients and Those with Disabilities Many GRATs include a so-called “swap” power in which the grantor is permitted to substitute assets of equivalent value with the GRAT. Handler is a partner in the Trusts and Estates Practice Group of Kirkland & Ellis LLP. Quintiles Transnational Corp.

Estateplanning is one of the most important steps in securing your financial legacy, but its also among the most complex. Understanding how assets will be distributed, navigating tax implications, and aligning these decisions with your personal goals can feel overwhelming.

There is something to be said for owning your own distribution channel,” he said. What works really well for us and going back to growth, referrals are too hard, all the steps in a referral, when you give them [advisors] a branded mobile app of their own that they can show, the response is often: ‘oh I want that,’” said Fields.

Traditional Investment Strategies The Role of Income Tiers and Priority Levels Case Studies Key Considerations Conclusion Introduction Waterfall Wealth Management is a financial strategy designed for high-net-worth individuals seeking a structured, prioritized approach to wealth distribution.

Each discussed how providing a more holistic approach to distribution-phase planning in their practices can amp up organic growth for advisory firms. Today, firms are using it to quickly build proposal decks and help advisors consolidate held-away assets. Now, two years in, it has built AI agents to automate document processing.

HSAs give you an upfront deduction for the year of contribution, grow tax-free, and distribute tax-free, making them one of the most powerful tax-advantaged accounts. Consider 529 Plans A 529 Plan is a tax-advantaged investment account specifically designed to fund education costs.

You mentioned donor-advised funds, uh, philanthropy when it comes to both financial and estateplanning. Philanthropy is a big part of both retirement and estateplanning. Asset allocation has called this the thorniest problem in all of finance. And you’re also doing a little bit of tax planning as well.

Below are some of the mistakes you should avoid making to secure your wealth: Mistake #1: Not diversifying your investments Investing too much of your money into one sector, one type of asset, or one region can expose your wealth to unnecessary risk. A good estateplan ensures your assets go where you want them to.

By planning for the unexpected, you can be confident that your family is prepared to weather any storms. Create a Will and EstatePlanEstateplanning allows you to outline precisely how your assets should be distributed and how your children should be provided for if you’re no longer there.

This approach typically provides greater benefits to those who have significant assets and high taxable income in retirement. Inheritance and estateplanning There are a couple ways a Roth IRA conversion can assist with estate and legacy planning. A spouse may also elect to defer RMDs if they inherit the account.

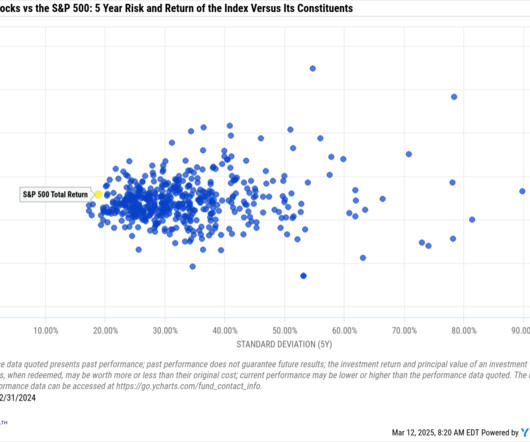

If one stock makes up more than 10% of your overall asset allocation, it’s probably too much. When considering the distribution of excess lifetime returns of individual stocks vs the Russell 3000, the median stock underperformance was almost -10%.(J.P. What is a concentrated stock position?

This can come from dividends, interest, rental income, and distributions from brokerage or retirement accounts. There are many ways to invest, including stocks, bonds, real estate, private equity, and alternative assets. Estateplanning: Structuring financial matters to align with personal preferences and long-term objectives.

For high-net-worth individuals, continuously refining your strategy over time is what keeps your plan efficient and aligned with evolving goals. She wants to minimize taxes while aligning her legacy with charitable values. They’ve built a solid savings habit, but now want to refine how their wealth is structured and protected long term.

Alternative investments encompass a broad range of assets beyond traditional stocks, bonds, and cash. Cryptocurrencies and digital assets: Decentralized digital or virtual currencies and other digital representations of value using cryptography. What are tax-efficient alternative investment structures?

They are essentially dedicated accounts into which you, and other donors as well, can place cash, stocks, or non-publicly traded assets that are eligible for an immediate tax deduction. You can take your time, however, deciding how you want to distribute the donations, which meanwhile can potentially grow tax-free within the account.

Vanessa is the CEO of Expressive Wealth, an RIA based in Chicago, Illinois, that oversees $135 million in assets under management for approximately 70 client households, including 10 ‘core' ultra-high-net-worth families.

Key deductions include: Mortgage interest payments on primary and secondary residences Property tax deductions (subject to SALT limitations) Home office deductions for qualifying spaces Maximizing Retirement Account Benefits Take full advantage of tax-advantaged retirement accounts to reduce your current tax burden: Contribute the maximum allowed to (..)

Your personal preferences and the potential good your bequests can do are factors to think about in your estateplanning. What Is Estate Equalization? Basically, estate equalization is the process of helping ensure fairness in your estateplan, whether that means leaving all your primary heirs the same bequests or not.

Roth IRAs offer unique advantages including tax-free growth, no required minimum distributions during the owner’s lifetime, and potential tax benefits for heirs. The absence of required minimum distributions during the owner’s lifetime. Some investors even convert stable-value assets first to minimize market risk.

What Are Qualified Charitable Distributions (QCDs)? For those over 70½, you might already be familiar with Qualified Charitable Distributions (QCDs). For years, QCDs have allowed people to donate directly from their IRAs without paying taxes on those distributions.

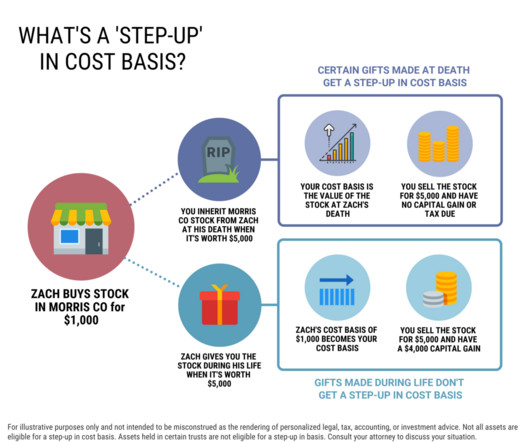

A step-up in basis is a tax advantage for individuals who inherit stocks or other assets, like a home. Heres how stepped up cost basis works on stock and other assets at death. Understanding step-up in basis at death If youve received an inheritance you may have questions about the tax treatment of certain assets.

By Brady Marlow, CFP, AEP, CAP, CPWA, CExP , Director, Carson Private Client Wealth Strategy Although most people focus first on loved ones in developing their estateplan, you may also want your legacy to include continuing support of issues and organizations youre passionate about. The trust is a wholly separate entity from you.

As a Christian, your estateplan should represent your dedication to financial stewardship according to Scripture. W hat important factors should Christians consider when estateplanning? W hat important factors should Christians consider when estateplanning?

In this article, well explore all the details of alternative investments, the reasons behind their growth as an investment choice, and how their tax treatment differs from traditional assets. Eligibility: Direct property investment does not require accreditation, but some real estate platforms have accreditation requirements.

And I think you will also, if you are at all curious about estateplanning or investing or personal finance, this is not the usual discussion and I think it’s very worthwhile for you to hear this and share it with friends and family. And suddenly you could buy index funds that cover all of the major asset classes.

Withdrawing money from your accumulated assets is often more complex than it appears. When you sell investments from these accounts, you may be required to pay capital gains tax on any profits, depending on how long you’ve held the assets and your overall tax situation.

Melissa Rodriguez June 11, 2025 5 Min Read As the most significant intergenerational wealth transfer in the history of the United States unfolds, women, particularly widows, are increasingly at the forefront of estate management and disputes.

When it comes to estateplanning, there are many pieces to ensure that your heirs and loved ones are taken care of and have a clear understanding of your wishes. Any estateplanning professional would tell you that the more you do while you are still living, the better.

trillion and 121 million participant accounts along part of the $37 trillion overall in retirement assets, the pressure is causing many record keepers to dig deep and, for many, reinvent themselves or face exiting the market before their valuations drop even further just as it did for active asset managers years ago.

No required minimum distributions (RMDs). For individuals with investments in assets such as stocks, real estate, and other securities, changes in the capital gains taxespecially long-term capital gainswill be particularly relevant. Enjoy tax-free growth and withdrawals. Drawbacks: Conversions may trigger taxes.

For executives and entrepreneurs holding highly appreciated assets, the need for diversification becomes increasingly important. But for those interested in charitable giving, there may be a way to address the tax concerns associated with highly appreciated assets and give meaningfully over time.

Asset and Liability Matching. Good financial planning is all about asset and liability matching across time. That means you need to make sure you understand how your income and assets relate to your expenses and liabilities. A financial plan with an asset liability mismatch is likely to fail over time.

Losing a spouse is a difficult time, and navigating the complexities of inherited assets can feel overwhelming. The Single Life Table typically results in higher mandatory distributions. Note that if the deceased account holder had not yet taken their RMD for the year of death, that distribution must still be taken.

If you choose to withdrawal early, youll often be distributed your proportionate value of your original shares, and such early withdrawal can result in the loss of tax deferral as well as fees or penalties imposed by the fund provider. The qualifying assets need to make up at least 20% of the portfolios total gross assets.

Consider investing in a mix of stocks, bonds, and other asset classes to spread risk and maximize potential returns. Protect Your Assets Protecting your assets is critical for preserving your financial security in retirement. Adjust your budget as needed to align with your financial goals and lifestyle preferences.

The second amendment to the revocable trust agreement directed the following distributions: • 2 million dollars to the trustee of the MCC Trust, to be held for Maria’s benefit. The MCC Trust agreement included terms about the distribution of trust assets: 3.2. Administration of Trust Estate for Beneficiary.

Key Takeaways: Net Unrealized Appreciation (NUA) is the difference between the cost basis of employer securities in a retirement plan and their market value at the time of distribution. NUA is not taxed as ordinary income at the time of distribution, which can offer significant tax advantages. What are the rules governing NUA?

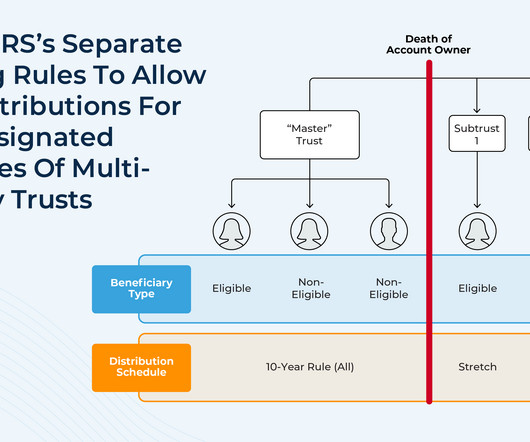

They might want to have more control over how the account assets are distributed to their beneficiaries. Whatever the reason, naming a trust as the beneficiary of a retirement account subjects the account to a complex series of rules regarding how the account must be distributed after the owner's death.

Resonant Capital Merges with Tax, Accounting Firm QBCo by Alex Ortolani Jul 18, 2025 1 Min Read SEC Chair Paul Atkins Alternative Investments SEC’s Atkins Says Changes to 401(k) Plans Must Be Reviewed Carefully SEC’s Atkins Says Changes to 401(k) Plans Must Be Reviewed Carefully by Nicola M. Handler, Alison E. 2d 369 (S.D.N.Y

Healthcare emergencies, unexpected home repairs, or the sudden loss of a loved one can shake up even the best retirement plan. Make sure you have at least a basic estateplan in place. Contribute to a Retirement Savings Plan A big part of how to prepare for retirement is putting your money to work.

Estateplanning is not just for the wealthy; it is essential for anyone who wants to ensure their assets are managed and distributed according to their wishes. A lack of estateplanning can lead to significant complications. An effective estateplan does more than simply divide assets.

Resonant Capital Merges with Tax, Accounting Firm QBCo by Alex Ortolani Jul 18, 2025 1 Min Read SEC Chair Paul Atkins Alternative Investments SEC’s Atkins Says Changes to 401(k) Plans Must Be Reviewed Carefully SEC’s Atkins Says Changes to 401(k) Plans Must Be Reviewed Carefully by Nicola M. Artists and authors don’t create fo.

morningstar.com) The biz Creative Planning was able to retain some 60% of the United Capital assets. riabiz.com) XY Planning Network is launching a new in-house RIA, XYPN Sapphire. obliviousinvestor.com) Estateplanning Changing an estateplan takes time. billion in donor-recommended grants in 2023.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content