This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ideally you’ve been rebalancing your portfolio along the way and your assetallocation is largely in line with your plan and your risktolerance. For example during the 2008-2009 market debacle I looked at funds to see how they did in both the down market of 2008 and the up market of 2009. Focus on risk.

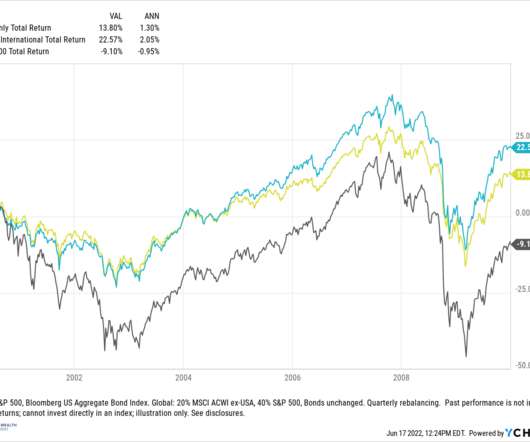

Between 2000 – 2009, the cumulative total return for the S&P 500 was negative 9.1% Since trying to time regime changes is very difficult in real time without the benefit of hindsight, there are reasons to consider allocating both U.S. equities to an assetallocation. These bouts can be significant. vs positive 30.7%

You can also get information on your performance and assetallocation. Like other similar products, they first determine your risktolerance, personal preferences, and investment goals. This will help you to create an assetallocation that will get you where you need to go with your investments.

We work with clients to create—either in writing or verbally—a “mission statement” detailing how they want their assets to serve their well-being in coming decades. This includes articulating a policy with regard to investment risktolerance, long-term goals, cash flow needs and sector diversification.

But our belief is that this economic and profit environment is better than in the early 1990s, early 2000s, or 2008-2009 and therefore supports higher valuations. We continue to recommend an overweight allocation to equities and underweight to fixed income relative to investors’ targets, as appropriate.

And what we figured out in 2009, really when we started buying homes is that we made the bet that it, I mean, it wasn’t a very exotic bet, but we made the bet that the subprime mortgage market wasn’t coming back at all. And so, so starting in 2009, we, we, there was no flip market. So it’s very long dated capital.

Barry Ritholtz : So I wanna wrap my head around a large insurer like MassMutual as a client, I would imagine very long term in perspective, but I don’t really grasp what sort of risktolerance an insurance company has. What is that sort of risk embracing, like how, how does that settle out?

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content