This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

An even tougher one, if you have medical issues, how expensive are they likely to be? I understand the difficulty of that one but if you're 50, overweight and taking a half dozen medications, you should plan on health stuff being very expensive. My 64 and 2 month number is $3049 which is where I get the $1524.50

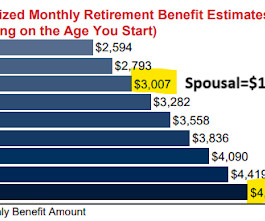

There are obviously plenty of people who retire while still having a mortgage but it's not totally unreasonable that someone could be mortgage free by the time they retire or maybe have their payoff date and retirement date coincide. This chart from the post was interesting.

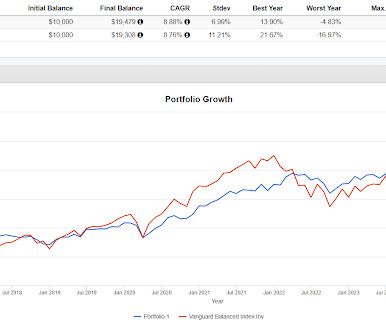

The example assumes no sort of serious medical or family calamity that altered your financial plan, life happens that way sometimes. I'd be happy with that standard dev number and lagging by 100 bps annually. If you're 81 and can no longer meet your income need from your portfolio, that is what matters.

But here’s the thing: whether you retire at 50 or 67, it isn’t just about leaving work, but being ready for what comes after. Start planning early. It takes strategic foresight, hard numbers, and smart decisions that begin well before your final day at work. Yet far too many professionals delay the planning process.

The Wall Street Journal looked at an issue near and dear to us by profiling four people who in middle age, had their hand forced into early or retirement or otherwise unexpectedly forced to find a new job. The first profile was a guy who was head of retirement research at Bank of America. I remembered to use the gift link.

A number of changes have been proposed and implemented since President Donald Trump returned to office. They can have a direct impact on the stock market, and by extension, on your retirement investments, including your 401(k). You must make room in your budget for these rising costs to keep your retirementplanning on track.

Retirementplanning for the self-employed can seem complicated and, often out of reach. Without a traditional workplace 401(k), many business owners and freelancers aren’t sure how to start putting money toward retiring someday. A payment plan of “substantially equal payments” over your lifetime. These include: 1.

One of those items on the estate planning to-do list is making sure your investment accounts and life insurance policies have their beneficiary designations filled out. However, it’s one of the most important aspects of estate planning.

Maybe my friend, or switch it around to her husband not liking his job, can retire at 62 and with the safety net of knowing he, or she, could take Social Security, can figure out how to monetize something else to maybe push back Social Security. Another friend is going through something very serious with a medical thing. million.

It’s about protecting yourself from unpredictable, rising medical expenses that could quietly dismantle even the most disciplined savings strategy. This article is a deep dive into healthcare costs in retirement. If you’re planning smartly for the long haul, this is where your attention should be focused. Beyond that?

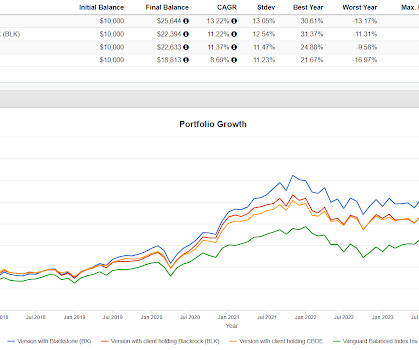

The kurtosis numbers are odd. Maybe they'll get it exactly right but I think it is prudent to plan now for something to go wrong between now and whenever benefits will supposedly be cut, that date is a bit of a moving target ranging 9-11 years from now. Most of the holdings I used are regulars in blog posts. No kidding.

Maybe people should focus less on hitting their retirementnumber versus hitting a workable number. million to retire at 66 and at 65 and a half you have $900,000, you gotta figure out how to make that work (save more, work longer, spend less, all three). Harshness coming but if you think you need $1.1

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirementplans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services. These “bundled” plans include Part A, Part B, and usually Part D. Consider your medical history and any ongoing conditions. Do I require regular prescriptions, and are they covered under my plan?

It’s important to note that some countries may require you to renew your visa regularly or meet residency conditions, like staying in the country for a specific number of months each year. Before choosing a country to retire in, review its residency rules thoroughly and make sure you meet the financial criteria.

Keep the following documents for seven or more years: Income tax returns (federal and state) W-2s and 1099s Medical bills Contracts Receipts for tax-deductible items Mileage records Canceled checks Real estate tax forms Credit cards statements that contain purchases used as tax deductions Retirementplan contributions.

2 Often, this is the first time that many Baby Boomers realize that decisions around Medicare aren’t just medical decisions; Medicare decisions also have significant financial implications. If they start their online application and receive a re-entry number, they can go back to Social Security to finish their application at a later time.);

The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years. Retirementplanning is not just about reaching a target savings number.

RetirementPlanning 5 Reasons Why Houston Is a Great Place to Retire Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. For many people, retirement offers the time and opportunity to travel and explore new endeavors they never had the time for during their working years. Is Houston a good place to retire?

When converting an hourly rate, like $25 per hour, to an annual salary amount, you need to start with the number of hours in your work week. Multiply 40 hours by 52 weeks to get the number of hours worked in a year: 40 x 52=2,080 hours 3. In the example below, we’ll use a standard 40-hour work week. Sample Calculation 1.

Financial professionals have a significant opportunity to address their concerns and help women plan and manage their financial journey. Inflation prevails among investor concerns Among women investors, uncertain market conditions – particularly inflation – have a rising number feeling unsure about their ability to retire at all.

From debit cards to your bank accounts and bank account numbers, and driver's license numbers, a lot of your personal information can be compromised. Someone may be trying to use your insurance for medical procedures or medicine. You should ask for any associated medical records and let your medical providers know.

Rising costs for health and medical care are also a factor in these purchasing decisions; almost half of adults say they are paying more for health care and medical expenses in the last 12 months. Another 14% said in the past year they put off or canceled plans to see a medical specialist because of high inflation.

Northwestern Mutual published a report about the state of retirement and of course all the numbers are grim. million to retire, up about 50% from 2020, while the average retirement account balance is $88,000. million, do you think that number is close to what you need? You can read about at Yahoo and Bloomberg.

Use Your Employer Sponsored RetirementPlan for All it’s Worth 5. It should come as no surprise that a disproportionate number of those are in the healthcare field, typically doctors of one type or another. But I whittled that list down to the top-paying positions that don’t require you to have a medical degree.

They both have decent-paying jobs, but their retirement savings are nonexistent. They have two kids, one of whom had significant medical problems as a young child. How and where they can best save for retirement depends on any number of different factors—do either or both of their jobs have any kind of retirement account benefits?

Focused Specialty Mint Hill specializes deeply in serving just one target population: professionals in the dental and medical fields. Authority Through Understanding The “Your Financial Journey” section demonstrates Mint Hill’s deep understanding of the unique needs of medical and dental professionals.

By weaving in extra savings into your spending plan, you can have enough money to cover gifts, cook your fancy holiday dinner, and keep the lights on (literally). . Max Out Your RetirementPlans. Saving for retirement should be as commonplace as meal prepping for the week. Let’s take a look at 2021 numbers. .

It laid out the threat and dug in with some numbers. I said it seems as though the food pyramid was created to sell us unhealthy, high margin junk food that makes us sick or worse so that we can then pay for medication to manage our sickness for the rest of our lives. I talked about this at fire training yesterday.

Included among your tax return items is $10,000 in medical expenses, along with other deductions (real estate tax, home mortgage interest, etc.) Your itemized deductions amount to $19,750 – because your medical expense deduction is limited to the amount over 7.5% and a number of miscellaneous credits. amounting to $15,000.

These professionals meticulously assess your financial situation, income level, and retirement goals to tailor personalized strategies. For instance, they can guide you on leveraging employer-sponsored retirementplans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts.

Personal Information Social Security Numbers (SSN) or Individual Taxpayer Identification Numbers (ITIN): Needed for you, your spouse, and any dependents for identification purposes by the IRS. Bank Routing and Account Numbers: Required for direct deposit of any refunds or for payments due.

Contributions can be deducted from your income and you can take money out without tax or penalty for qualified medical expenses. A big benefit that doesn't get talked about enough is that there is no time limit to take money out for a qualified medical expense. Here's an example of what I mean. Will it be worth it?

If you wish to have a firm grip on your finances and want to learn about different strategies related to investing, tax-saving, or retirementplanning, consult with a professional financial advisor who can advise you on the same. You need to review your financial plan at regular intervals.

Financial security is when you have enough financial resources to cover basic needs and unexpected expenses, such as medical bills. 4 Milestones to financial independence Having financial independence means that you can retire early or pursue your passions without being held back by financial constraints. What about financial security?

Your gross income determines the number of figures you earn. A budget will help you gain clarity on your income and expenses, prioritize where your money should go, and help you create a plan of action. Let’s assume that this number is $65,000 per year or $5,416 per month. A two-figure number has two digits — like 45.

There are four parts to Medicare plans: Part A: Hospital insurance. Part B: Medical insurance. This penalty is proportional to the number of years you were eligible for coverage but didn’t use it. For more information on the retirement mistakes to avoid, contact us today. . |. The Four Phases of Retirement.

Further, if both spouses have a considerable number of individual tax deductions, it may be advised to file your taxes separately and claim the deductions individually to get a better tax cut. Retirementplanning is a must, so start with maximizing your 401k and Individual Retirement Accounts (IRAs). To conclude.

As was the case for 2022 we're saving about $1000/mo because we can get away with catastrophic coverage and by Blue Cross' estimate, another $500/mo on other medical expenses. For years, I've tried to make the point here that staying healthy has direct cause and effect financial benefits.

By weaving in extra savings into your spending plan, you can have enough money to cover gifts, cook your fancy holiday dinner, and keep the lights on (literally). . Max Out Your RetirementPlans. Saving for retirement should be as commonplace as meal prepping for the week. Let’s take a look at 2022 numbers. .

While the future can be unpredictable, the five to ten years before retirement are a great time to get a realistic picture of your lifestyle costs. At that point, you likely have a clearer understanding of what it takes to maintain your current standard of living, and that can be the starting point for your retirementplanning.

How much should you be saving for retirement in your 20s? How do I start putting money away for retirement? Articles related to preparing for retirementRetirementplanning in your 20s: Start saving now! The great thing about the 401(k) plan is that you get to save the maximum amount of your income before taxes.

Those numbers make it clear that farmers are generally not retiring at age 65. Helping navigate the Medicare enrollment process by making sure your farmer-clients sign up at the right time and select the right type of Medicare plan(s) is a crucial task. Retirement Income and Transition Planning in Agriculture.

The sorts of things that inhibit our ability to work longer are all things you've heard before including ageism which can include a lot of different things, some sort of medical or physical issue or some sort of burnout. I would also start to Plan B some ideas if the thing(s) you're relying on doesn't pan out.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content