This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The post Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility appeared first on Yardley Wealth Management, LLC. Staying Disciplined: How to Stick to Your Financial Plan Despite Market Volatility Introduction: Market volatility is a fact of life for investors.

The choice between stocks and bonds depends on their individual circumstances, such as risktolerance, time horizon, and financial goals. While an investor’s timeline affects their risktolerance and allocation decisions between stocks and bonds, it’s important to remember how long a retirement time horizon can truly be.

Risktolerance and asset allocation? It helps you balance risk and reward based on your goals and timeline. RiskToleranceRisktolerance is your comfort level with investment swings—whether you can stomach market dips for potential gains or prefer steady, safer returns.

Investing for Retirement: Strategies for Long-Term Success Introduction Investing for retirement is a journey that demands careful planning, patience, and discipline. Do you plan to travel extensively, pursue hobbies, or volunteer? Learn more about retirement plan options here. What lifestyle do you envision?

You can choose something standard, have a standard portfolio tailored slightly to your needs, or have an investment advisor build a portfolio just for you based on your resources, needs, goals, timeline, risktolerance, current market conditions, and more. These are the basic building blocks of any portfolio.

Economic Update: Market reaction: The sell-off reflects uncertainty, not full confidence that the tariffs will hold negotiations are expectedarket reaction: The sell-off reflects uncertainty, not full confidence that the tariffs will hold negotiations are expected. Actual economic or market events may turn out differently than anticipated.

In 1916, the number of stocks represented by the DJIA increased to 20 and remained at that level until moving up to its current 30-count in 1928 to reflect the (soon-to-end) economic boom of the Roaring 1920s. Any investment should be consistent with your objectives, time frame, and risktolerance. stock market index.

Market downturns can bring uncertainty, and with recent headlines about tariffs and economic shifts, you may be wondering whats next. Just weeks ago, analysts were predicting continued market growth, and now, concerns about global trade and economic conditions are leading to increased volatility.

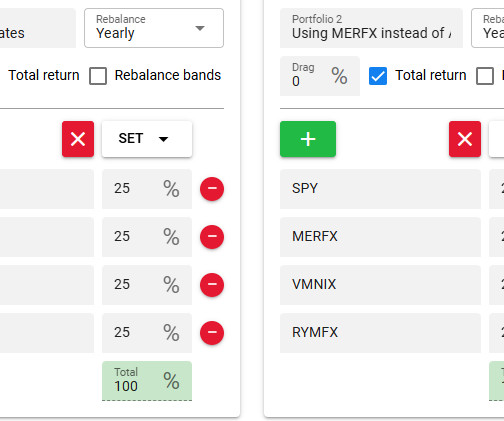

They talked about "four pillars" as being "economic growth (equities), income defensiveness (bonds), absolute return (alpha) and trend following (tail risk)." Research Affiliates (RA) threw its hat in this ring with a long writeup about managed futures. Portfolio 1 is an attempt to be true to the RA paper using AGG for bonds.

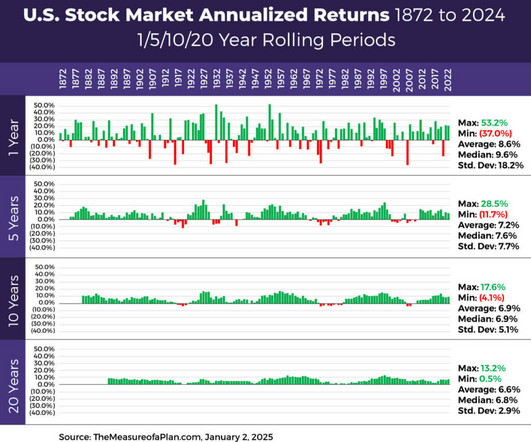

Diversification to Spread Your Risk Diversification is an approach to help manage, but not eliminate, investment risk in the event that security prices decline. By its nature, diversification is designed to align an investor’s goals, time horizon, and risktolerance. The Measure Of A Plan, January 2, 2025 [link] 6.

As a result, they may not survive economic downturns as easily, and their stock prices can be a lot more volatile. You can diversify your portfolio inside your retirement account and even adjust it as your risktolerance or goals change over time. In some cases, it may also be exempt from state and local taxes.

With constant headlines about market swings, economic policy changes, and financial uncertainty, its easy to feel overwhelmed. Having an experienced financial advisor by your side can help you stay grounded in your plan, even when markets feel anything but steady. Your financial plan is designed for the long term.

IBM has announced that it plans to invest $150 billion in the U.S. So, if you are planning your next investment move, speak to a financial advisor about the future of AI and other tech enhancements. So, even with ETFs and futures making access easier, it is essential to know your risktolerance and investment goals before jumping in.

The “whiplash theme” of the current administration’s economic agenda necessitates investor readiness to adjust to sudden changes in fiscal policy. Uncertainty and unpredictability given the difficulty of economic forecasting due to the unusual level of policy influence in the market right now. The bottom line?

Which means that longer-term projects, such as creating a succession plan to have in place for the firm when the owner retires, may tend to get put on the back burner.

Our relationship with money is complicated: Speak to someone at the bottom of the economic ladder and they will tell you in no uncertain terms that a lack of money can lead to misery; but speak to enough millionaires and billionaires and it’s pretty clear that money doesn’t automatically lead to happiness.

When it comes to their investment portfolios many tend to have a low-risktolerance and with the unsettling economic situation with the ongoing pandemic, the word “risk” has become even more of a fearsome word for clients. This will allow you to get a general sense of where your client’s risktolerance stands.

Among these are your longevity, lifestyle, comfort with market performance, sequence of return risk, current health, housing plan, proportion of fixed to variable expenses, proximity to children and so much more. often fail to consider sequence of return, housing, longevity, health or family risks faced in retirement.

The Imperative of Estate Planning: Not Just for the Affluent Often, there’s a prevailing misconception that estate planning is a luxury reserved for the wealthy elite. Real estate planning is a crucial undertaking that every adult and family should prioritize. This notion couldn’t be further from the truth.

When putting a plan in place, we believe it is critical for any mission-driven organization to develop an effective, long-term asset allocation strategy to manage its endowment assets. RISK AND RETURN. By contrast, the risktolerance of an organization is more variable and will depend entirely upon its unique needs and preferences.

That’s because each investment strategy will apply in different economic and financial environments. Traditional IRA: Best for Dedicated Retirement Planning. IRA plans are subject to Required Minimum Distributions (RMDs) beginning at age 72. Roth IRA: Best for Retirement Planning + Immediate Funds Access. How to invest.

Prices can go from all-time highs to major lows in just a few days, all thanks to global economics, interest rates, and political happenings. Bear markets signify a downward trend in stock prices , often triggered by economic recessions, political uncertainties, or market saturation. When is a good time to invest in the stock market?

2022 Year-End Planning Letter: Reflections and Perspectives ajackson Mon, 11/28/2022 - 11:10 The end of the calendar year is traditionally a time of reflection, and for us it is a chance to sit with clients, review progress, discuss the events shaping the investment landscape, and revisit goals for both the near term and the long term.

2022 Year-End Planning Letter: Reflections and Perspectives. Meanwhile, the global economy has been deeply impacted by the confluence of all of these events; the most significant near-term result, in our view, has been the return of inflation as a truly global economic threat for the first time in decades. Mon, 11/28/2022 - 11:10.

Invest in the Stock Market Suggested Allocation: 40% to 50% Risk Level: Varies Investing Goal: Long-term growth The stock market is where most of us save for retirement already, mostly through the use of tax-advantaged retirement plans, like a 401(k), SEP IRA, or Solo 401(k). Are you hoping to turn a quick profit instead?

This advanced language processing technology has also greatly impacted the financial advisory sector, prompting a critical question: Can ChatGPT replace human financial advisors in retirement planning? Personalized guidance, empathy, and a deep contextual understanding are integral to effective retirement planning.

They are professionals who hold specialized degrees or certifications in finance, economics, or related fields. Their knowledge extends to various investment products, risk management, tax implications, and financial planning. Investment advisors stay updated with market trends, economic conditions, and geopolitical events.

Recognizing the need for a financial plan is a significant first step toward the goal of achieving personal financial security. Table of Contents What is a Financial Plan? Table of Contents What is a Financial Plan? Why is Financial Planning so Important? Why is Financial Planning so Important?

Recessions often arrive unexpectedly, even for investors tuned in to the latest economic news. When a rough economic patch appears on the horizon, your clients seek your guidance to help them check their emotions and stick to a strategy to help them manage market risk. Diversify your client’s income sources.

Economic headwinds and market fluctuations make the anxiety even worse for investors close to retirement. Maintaining an appropriate asset allocation for an investor’s specific goals and risktolerance is critical for long-term success. Many near-retirees see their highest portfolio values just before retirement.

For instance, they can guide you on leveraging employer-sponsored retirement plans, such as a 401(k) with employer matches, to optimize your contributions and harness the full benefits of the accounts. IRAs offer you the flexibility to contribute to your retirement savings independently, outside of employer-sponsored plans.

Focus on Financial Preparedness: Regardless of external factors like the debt ceiling, it’s always wise to have a robust financial plan in place. By having a strong financial foundation, you can better weather any potential economic fluctuations.

And so, coming out of school, I studied Economics and Spanish Literature, and I applied to a — a program that actually targeted Liberal Arts majors. You have a background, undergraduate, your economics degree from Notre Dame, but you were dual-major Spanish language and Literature degree, how useful was that in Latin America?

Their primary objective is to help clients make informed investment decisions, manage risks, and achieve financial objectives. Investment advisors analyze market trends, assess the client’s economic situation, and develop personalized investment strategies tailored to their goals and risktolerance.

A recession is defined as a temporary period of economic downturn. A country is considered to be in recession if its Gross Domestic Product (GDP) has witnessed negative economic growth for two consecutive quarters. A recession is a stage in the economic cycle that is bound to recur over time.

Others think that you should try to time things so that when a market or economic conditions are a certain way, you should try to do things differently. Otherwise, keep your portfolio as it is as long as that portfolio allocation makes sense for you. Rebalance it, don’t change, and don’t try to time things with the market.

The answer lies in smart and strategic retirement planning. It’s time to rethink when to start stashing away those savings and how to modify your plan in a world that’s constantly changing. Consider consulting with a financial advisor who can help devise a personalized retirement plan based on your unique needs and goals.

As we continue to deal with record-high inflation and economic instability, you might be wondering how you should manage your investments. The way you set up your portfolio should reflect your risktolerance and goals, and be revisited once or twice annually to make sure it’s still on track. . About Your Richest Life.

Like any investment, the value of your Roth IRA can fluctuate due to changes in the stock market or other economic conditions. It’s important to consider your investment goals and risktolerance when deciding how to invest your Roth IRA. Now we have that clear, here’s some ways you could lose money in a Roth: 1.

It ensures that your portfolio aligns with your risktolerance and enables you to establish the desired equilibrium between stocks and bonds. This helps you maintain a risk profile that resonates with your financial goals. Major life events often coincide with changes in your risktolerance.

Robo-advisors offer easy account setup, robust goal planning, account services, and portfolio management all at a reasonable price - start investing today by clicking on your state. Ad Online Financial Advisors are ready to provide you with quality economicplanning and investment management. Investing with a Plan.

Assess your risktolerance: Cryptocurrencies are known for their volatility, with prices that can fluctuate significantly in a short period. Define your investment goals: Think about how investing in cryptocurrencies fits into your overall financial plan. No credit risk Investing in precious metals doesn’t involve credit risk.

While there may be alternate exercise methods such as a cashless exercise, it’s essential to know that this might be an issue in the future, and planning for the proper funding of an exercise can prevent cash flow issues and unpleasant tax implications in the future. Understand Your Investment RiskTolerance.

This data can serve as a baseline for tailoring your retirement plan, taking into account factors such as inflation, your current age, and your desired retirement age. This article also explores the average monthly spending habits of individuals aged 65 and older and offers practical insights to help structure your retirement plan.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content