This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

million next year) to $15 million in 2026, and raising the limit on the deductibility of State And Local Taxes (SALT) to $40,000 (though this measure is scheduled to revert to the current $10,000 in 2030 and begins to phase out for consumers with more than $500,000 of income), among many other measures.

From there, we have several articles on investments: How Morningstar plans to simplify its rating system amid continued concerns about its effectiveness. A study suggests that some fund companies are misleading investors by changing their benchmark indices to make their performance look better.

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

Petersen, CPA, CFP ® , CP, Affluent Wealth Planning The holidays are upon us! That must mean it’s time to roll up my sleeves and get to work on year-end financial planning – with an emphasis on 2023 income tax. Lastly, I allocate the retirementplan contributions between Roth and Traditional 401(k) accounts.

Tax planning might not top everyone’s list of leisure activities, but in the middle of tax season, theres a hidden opportunity. Harnessing Tax-Advantaged Savings Retirement accounts and health savings plans offer the dual benefits of saving tax and building wealth.

Some of the measures in the bill include increasing the required minimum distribution age, raising catch-up contribution limits, permitting some rollovers from 529 plans to Roth IRAs, and expanded access to employer plans. retirement changes. Starting in 2026, the catch-up will be indexed by inflation. The Secure Act 2.0

Although a number of these provisions will negatively impact taxpayers starting in 2026, there a few changes that will be positive. Here’s a summary of the major tax law changes coming in 2026 and some steps individuals and business owners can take to prepare. In 2026, this is all expected to change (again).

These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement. 401(k) Plans: Contribute the maximum allowable amount for 2024 : $23,000 if youre under 50, or $30,500 if youre 50 or older.

A lot of people out there dream of early retirement – who wouldn’t love to hang up the office keys and jump off the 9-5 train sooner rather than later? But while it’s possible to retire at 50 and have plenty of time left in life to have new experiences, it takes careful planning and a will of steel.

in 2026, the eligibility age will be adjusted to 46. The beneficiary may only make this contribution if they are not participating in any employer sponsored retirementplan. The current tax law also allows for a rollover from a 529 plan to an ABLE account up to the annual limit amount. With the passing of Secure Act 2.0,

Additional ways to fund a Roth IRA For workers with access to a 401(k) or other qualified retirementplan, a designated Roth account can be a fantastic opportunity to create a larger Roth account balance for retirement. Let’s further assume that this is after $10,000 in pre-tax contributions to a traditional 401(k) plan.

in 2025, 8% in 2026, 7.8% Part G Medicare, the one I believe to be the most robust supplemental plan currently costs an average of $1517/yr with projections of 10+% increases over the next few years. "Currently, retirees with modified adjusted income below $97,000 pay $1,979 a year in Part B premiums. in 2024 and 6.2%

Most professionals approaching retirement know they need a plan. What many underestimate (often drastically) is the size of the piece of that plan that should be devoted to healthcare. Retirement is no longer just about 401(k)s and Social Security. This article is a deep dive into healthcare costs in retirement.

Seeking professional advice can provide valuable insights and a roadmap to achieve your financial goals with strategic planning. An effective financial advisor should be proactive in reviewing your tax plan before the year-end. Developing a plan to navigate the complexities of Social Security taxes is essential.

By Ryan Egolf, EA, Senior Tax Planner As the New Year quickly approaches, it’s time to put a bow on your 2023 financial plan. While this is by no means an exhaustive or comprehensive list of financial planning tools, these three broad areas will get you headed in the right direction. Rates are more accessible than ever before.

For example, they could make most of their charitable contributions and medical expenditures in a year they plan to itemize. In 2026, the current larger exemption will be reduced from $12,920,000 in 2023 to about $6 million per person ($5 million per person adjusted for inflation). Also consider the capital gains rates brackets.

just upended retirementplanning…again. The age when retirees must begin drawing from non-Roth retirement accounts increases to 73 in 2023, then 75 in 2033. Raising the age when withdrawals must begin is great as it gives investors more planning opportunities. The Secure Act 2.0

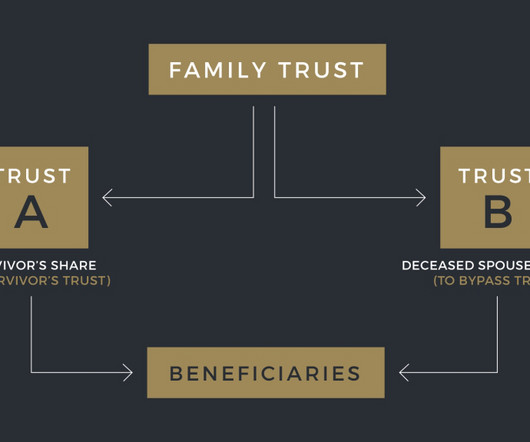

Has it been nearly a decade (or more) since you and your spouse updated your estate plan? If so, there’s a good chance your plan includes the classic “AB Trust” structure, which—prior to 2011—was the primary way for married couples to double the value of their federal estate tax exemptions.

without a scheduled sunset) the lower individual tax rates enacted as part of the Tax Cuts and Jobs Act (TCJA), and maintaining the estate tax exemption at TCJA-prescribed levels (which would reach approximately $15 million in 2026), there are several differences between them (e.g.,

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content