This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In the early days of wealth management, a financial advisor's value proposition was relatively explicit, typically focusing on a limited range of portfoliomanagement activities (e.g., selling and trading) or on sales-oriented advice that centered on implementing insurance products.

Real estate riskmanagement: Your primary residence, commercial properties, etc., These accounts typically offer stronger privacy protections as well as favorable tax regimes that can enhance your wealth preservation strategy. So, take calculated risks, research well, and consult experts as and when needed.

There are countless, valid approaches to portfoliomanagement but if you pick the right stock or niche, the fundamentals don't unravel and it continues to do what you'd expect it to do, why would you get out of the position? Maybe you trim a little for riskmanagement but that is different than getting out completely.

The course covers an introduction to personal finance, credit cards, life insurance, health insurance, investment instruments, loans, income tax and planning, budgeting and building a strong portfolio. Also, you will learn how to plan your taxes, credit score importance and how to budget your income to create a portfolio.

Wealth management is an important aspect of the financial world that focuses on managing wealth to help individuals and families achieve their financial goals. Wealth management involves a range of financial services as an investment, finance, real estate, tax, and riskmanagement.

We learned everything, you know, across from accounting to auditing to, to tax and valuation. So our analysts and our firm are as important as our portfoliomanagers. 00:24:18 It’s not necessarily as track to portfoliomanagement. What we want to protect against is unintended risk.

At its core, the CFP® Fast Track equips you with the expertise to offer sound financial advice, specializing in areas such as retirement planning, riskmanagement, tax planning, and wealth management. By pursuing this course, you become proficient in helping individuals and companies achieve their financial goals.

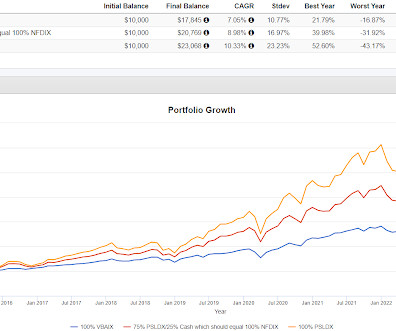

Some portfoliomanagers might very well be constrained that they have to own bonds, chances are you are not constrained in that manner. I have mentioned a predecessor fund the Corey (or Corey's company) managed, the Newfound RiskManaged US Growth Fund which recently closed, it had symbol NFDIX.

Financial RiskManager (FRM) – If you love solving problems and wish to help your clients mitigate risks you can turn your attention to a career as a Financial RiskManager. You can also undertake the globally recognized course in riskmanagement from GARP (Global Association of Risk Professionals).

Tax Considerations Be mindful of tax implications related to your goals. Certain investments or strategies may offer tax advantages, while others could result in higher tax liabilities. Consulting with an advisor can help you optimize your financial plan along with identifying the impact of potential future tax changes.

Dear Zoe Experts, I’ve been looking for tax planning guidance and am deciding whether to hire a financial advisor or an accountant. Financial advisors focus primarily on investments, while accountants focus more on taxes and other record-keeping aspects of finances. You’re on the right track!

Some common career paths for investment advisors include working as wealth manager, family office, portfoliomanager (PMS), Retirement Planner, Estate Planner. Investment advisors can also specialize in specific areas such as retirement planning, tax planning, or portfoliomanagement.

Tax Considerations Be mindful of tax implications related to your goals. Certain investments or strategies may offer tax advantages, while others could result in higher tax liabilities. Consulting with an advisor can help you optimize your financial plan along with identifying the impact of potential future tax changes.

Corporate bonds provide higher yields but vary in risk based on the issuer’s credit rating. Municipal bonds offer tax advantages, particularly beneficial for high-income retirees. High-yield bonds can enhance returns but carry greater default risk. Bond diversification Government bonds (e.g.,

Certified Financial Planner This course will help you better to understand the basics of personal finance, budgeting, investing, credit, taxes, and more, whether you’re a beginner or an Commented [RPSN1]: Certified Financial Planner advanced financial planner. Here are some options: 1.Certified

You have the liquidity, the tax efficiency, the transparency. BERRUGA: We think it’s a great solution for clients that are looking for two things, either income or like a riskmanagement tool to play the volatile environment that we have seen in the markets. I was already an investor in ETFs at that point in time.

The scope of wealth management goes beyond traditional financial planning and investment advisory services, encompassing a more holistic approach to personal finance. Wealth managers collaborate with their clients to develop customized strategies for asset allocation, tax planning, estate planning, and riskmanagement.

Remember, each strategy has its pros and cons so the best way to maximize them is working with a financial planner who’ll help your portfolio reflect the right risk with your financial goals. Diversification is a riskmanagement strategy that seeks to ensure your portfolio isn’t over- or underexposed in a certain area.

Plus, putting charitable giving in the context of other wealth planning strategies like estate and tax planning can help increase the effectiveness of your philanthropy and overall financial plan. A recent survey of donors and nonprofits found that one in five projects are negatively affected by risk. [1]

And Wall Street didn’t work out for a variety of reasons, but I ended up working sort of an adjacent industry in the portfoliomanagement software business, and really wasn’t where my passion was. They’ll construct the portfolio. They’ll do tax planning, right? And they bring a lot of value, right?

So how do you then go from tax and audit practice to finance and investing? If I’d moved to Hong Kong, I think it would have looked like a fairly self-serving tax trade. We just get to focus on assets and asset riskmanagement. So earlier we were talking about assets, and then you referenced riskmanagement.

She was a partner and a portfoliomanager at Canyon Capital, a firm that runs currently about $25 billion. Even the guy you think of so highly, you know, after three hedge funds open and close, you got to wonder if there’s some riskmanagement issue there. MIELLE: — interviewed. But that’s the thing.

But it was a tremendous experience because I had started off in bond trading, worked my way into portfoliomanagement and running the bond indexing team for a number of years, and then I got asked to take this responsibility, which was much broader. Also being cognizant of the tax implications of trading activity.

[Barry Ritholtz] : 00:17:05 [Speaker Changed] The, the rule to be tax exempt in the US is you have to disperse 5% of the foundation. You don’t have to pay any tax and just let the rest ride. And the third, the one that nobody talks about is riskmanagement. Riskmanagement. You give out 5%.

Macchia mentions that there are firms that have sprung up offering no load products, products that report into your portfoliomanagement system, wrap-able products, etc. Macchia chimes in, saying he finds it ironic that the first module in the CFP program is riskmanagement, which he interprets to be about insurance.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content