This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In a bull market, protecting one's downside gets punished, and after being burned enough times, people tend to lighten up on riskmanagement, or abandon it altogether. In a bull market the more risk you take, the more you're rewarded, and the more you're rewarded, the more you forget about risk.

00:14:50 [Speaker Changed] Yeah, it was about the middle of 2009. And then as we got into 2009, companies were starting to sort out, you know, where they were. And that’s, and it was about mid 2009 where ING decided to take, take the state aid. What we want to protect against is unintended risk.

We are currently experiencing one of the most volatile times in decades, on top of the start of the pandemic and the 2008-2009 recession. That’s why, when facing market volatility, stewards of long-term assets held at all types of nonprofit institutions recognize the importance of a well-thought-out investment process. .

So a very different dynamic than we saw back in 2007, 2008, 2009. So obviously, riskmanagers, you know, and CROs were very focused on how do we manage that risk and diversify that credit risk that they were taking on in mid-market companies. Yes, there’s a lot of liquidity in private equity.

KOENIGSBERGER: What I really like is on top of these four return streams that we have, we kind of have a multi-asset, dynamic assetallocation process. KOENIGSBERGER: So that’s what — with our multi-asset strategy, we wanted to solve for that problem, which is — I call it a governance problem.

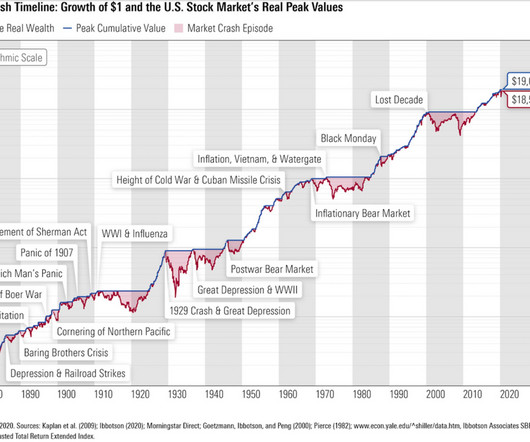

The DJIA closed 1999 at 11,497 and 2009 at 10,428. At the GFC bottom, March 9, 2009, the Dow traded at 6,547. ” That may have been a perfectly appropriate assetallocation for Professor Markowitz, of course, but his thinking was far more fear-based than analytically driven. So, he missed it by a mile.

And what we figured out in 2009, really when we started buying homes is that we made the bet that it, I mean, it wasn’t a very exotic bet, but we made the bet that the subprime mortgage market wasn’t coming back at all. And so, so starting in 2009, we, we, there was no flip market.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content