This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

In this episode, we talk in-depth about how Travis originally developed his specialization of student loan planning through first correcting the misinformation given to his (now-)wife and her friends in the medical field (and realized that he could give high value to a chronically underserved population), how Travis first started his student loan consulting (..)

An even tougher one, if you have medical issues, how expensive are they likely to be? I understand the difficulty of that one but if you're 50, overweight and taking a half dozen medications, you should plan on health stuff being very expensive. My 64 and 2 month number is $3049 which is where I get the $1524.50 number for her.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. What’s the earliest you can retire?

Whether it is a job loss or a medical emergency, the fund acts like a safety net, so you do not have to rely on high-interest debt. Once you have a number, multiply it by six. The red numbers in your portfolio are only losses on paper. But what if you are in your 60s or 70s and getting ready to retire?

Common deductions cover a wide range of expensesfrom mortgage interest, charitable contributions, to medical expenses exceeding 7.5% These include student loan interest, educator expenses, and certain contributions to retirement accounts. Medical and dental expenses exceeding 7.5% of your AGI. Why do tax credits exist?

The Retirement Manifesto Blog had a post about the "5 Top Regrets of Retirees." Retiring with too much debt? If you have a lot of consumer debt, and assuming no sort of horrible medical event you're paying for, then sorry, you're living beyond your means. The first regret was not saving enough money.

The people who undergo an audit have been selected due to a number of red flags that the IRSs computer-based system has detected. Common mistakes that can trigger an IRS audit There are a number of key red flagsranging from mistakes made on tax returns to specific financial circumstancesthat can attract IRS scrutiny.

Want to retire early? You can accomplish this task in several ways like strategic charitable giving, maxing out your retirement accounts, tax-loss harvesting, and more. Your emergency fund protects against unforeseen circumstances like job loss, medical bills, unexpected travel, home malfunctions, and more.

The example assumes no sort of serious medical or family calamity that altered your financial plan, life happens that way sometimes. I'd be happy with that standard dev number and lagging by 100 bps annually. If you're 81 and can no longer meet your income need from your portfolio, that is what matters.

The value of the S&P 500 index of stocks, where most of us hopefully have a good chunk of our retirement savings stashed into index funds, is up about fifty seven percent in just the past two years. Does this make it more vulnerable to a huge crash in the future, and will it affect my retirement? 4.3% – 5.3%

The Wall Street Journal looked at an issue near and dear to us by profiling four people who in middle age, had their hand forced into early or retirement or otherwise unexpectedly forced to find a new job. The first profile was a guy who was head of retirement research at Bank of America. I remembered to use the gift link.

Weaving in an article from Yahoo about Americans flunking a six question retirement quiz, "most respondents bombed big time" the article said. Beliefs about retirement are our own race, our own thing to figure out for ourselves. We all know people very well prepared for retirement and people who would appear to be in a lot of trouble.

Barry Ritholtz : The the funny thing is, the behavioral aspect of mutual funds seems to have been when people finally learn about a manager who’s put up great numbers, by the time it makes to make makes it to Forbes, hey, most of that run is probably over and a little mean reversion is about to kick in.

A number of changes have been proposed and implemented since President Donald Trump returned to office. They can have a direct impact on the stock market, and by extension, on your retirement investments, including your 401(k). How do tariffs affect retirement savings and 401(k) , and what can you do about it 1.

A number of TCJA provisions are set to revert to pre-TCJA levels or disappear entirely, impacting both individuals and businesses. While the exact income thresholds will be adjusted for inflation, the number of brackets and the corresponding tax rates will change. Note the permanent medical expense deduction threshold: The 7.5%

Retirement planning for the self-employed can seem complicated and, often out of reach. Without a traditional workplace 401(k), many business owners and freelancers aren’t sure how to start putting money toward retiring someday. There are, of course, individual options available, specifically Roth and Traditional IRAs.

You likely give some thought to selecting a beneficiary after starting a new job when you enroll in your companys retirement plan, but then it probably fades into the back of your mind since no one likes to dwell on their mortality. However, it’s one of the most important aspects of estate planning.

Most professionals approaching retirement know they need a plan. Retirement is no longer just about 401(k)s and Social Security. It’s about protecting yourself from unpredictable, rising medical expenses that could quietly dismantle even the most disciplined savings strategy. Healthcare in retirement isn’t a single bill.

But we’re already seeing the results: businesses are bracing for massive changes, currencies and interest rates are reacting, and regular investors like you and me are wondering what the future holds for our early retirement funds. So what’s the real answer? And that’s where our current tariff regime gets it completely backwards.

The kurtosis numbers are odd. Yahoo Finance had a cleverly titled article; Generation X is gloomy, but their retirement reality may not bite. Taking fewer medications while retaining the ability to bend down a lift heavy things will give us more optionality and resiliency. Most of the holdings I used are regulars in blog posts.

Yahoo wrote about the biggest regrets that people had about retiring. Sprinkled in there of course were some grim average and median retirement account balances. Maybe people should focus less on hitting their retirementnumber versus hitting a workable number. Retiring with too much debt was on the list.

He began his career as a medical doctor, a neurologist who discovered he had a knack for investing and investment research, eventually opening Efficient Frontier Advisors. You went to medical school. And so I realized I was going to have to invest and save for my own retirement. His most recent book is The Delusions of Crowds.

Number 8860726. Over 57 million individuals are currently over age 65, and that number will climb to an estimated 88 million by 2060. 2 These individuals often face chronic conditions such as Alzheimer’s disease, which affects more than 6 million Americans, a number that’s projected to triple by 2050.

Retiring or furloughed before age 65 is a long-term goal or a dire situation for many older workers who find themselves in the middle class these days. With the exception of many government workers and military retirees, health insurance and its attendant cost is the number one worry for early retirees, either by design or default.

Retiring abroad can be a dream come true for many Americans, offering the opportunity to explore new cultures, enjoy different climates, and potentially stretch retirement savings. Taxes One of the biggest financial considerations for Americans retiring abroad is understanding how taxes will work. tax return every year.

At the same time, the study found that potential breakaway brokers view the operational and compliance requirements of transitioning to and doing business as an RIA as a major concern, which could lead some of them to either leverage the growing number of service providers available to RIAs, or perhaps join an existing corporate RIA platform to take (..)

A recent study shows that while many consumers have expressed an interest in ESG investing, such funds within retirement plans have received limited allocations from investors. A survey showing how millionaires allocate their assets and the importance they place on the recommendations of their financial advisors.

However, choosing the right Medicare plan is crucial to ensure that you have the coverage you need as you move into retirement. Part B (Medical Insurance): Covers certain doctors’ services, outpatient care, medical supplies, and preventive services. Consider your medical history and any ongoing conditions.

Northwestern Mutual published a report about the state of retirement and of course all the numbers are grim. million to retire, up about 50% from 2020, while the average retirement account balance is $88,000. million, do you think that number is close to what you need? You can read about at Yahoo and Bloomberg.

When putting away for retirement, we often dream about all the things we’ll be able to do with that money – traveling, going out to eat, maybe trying new hobbies. . Of course, there are always the everyday household expenses to account for in your post-retirement budget. 1 It’s a number that just keeps rising, too.

Starting early with investing for retirement is so important to secure your future self. This means that saving for retirement should be a component of your overall financial portfolio and wealth-building strategy. So, let’s discuss how to save for retirement in your 20s! How do I start putting money away for retirement?

1 It’s important to have these conversations – and it’s vital to have them before cognitive decline or a medical emergency occurs. Information you’ll want to document includes: Bank accounts Investments Retirement accounts Estate planning documents (wills, trusts, etc.)

Saving money is an important task at any age, but as you hit your 40s, the need to save for retirement grows. While savers in their 40s and 50s typically have a decade or two left to save for retirement given the traditional age of 65, emphasizing saving now can set you up for a dream-worthy retirement.

Navigating the journey to retirement can often feel like a complex puzzle, especially when it comes to figuring out how much you need to save. The answer to “how much you need to retire” is shaped by various factors, including the kind of retirement life you dream of, your age, and the expenses you anticipate during your retirement years.

Writing for Bloomberg, Allison Schrager suggests that in order to enjoy retirement, we should work a little longer. Ann Tergesen at the Wall Street Journal reports that while most people expect to retire at 65, 62 ends up being more like it. I haven't even mentioned coming up short in retirement savings. Summing up Schrager.

Is medical underwriting required to qualify for a Medigap policy? No, during the initial enrollment period for Medicare Part B, medical underwriting is not required to qualify for coverage. Medical underwriting may be required and could result in either denial or higher premiums. Can I change Medigap companies in the future?

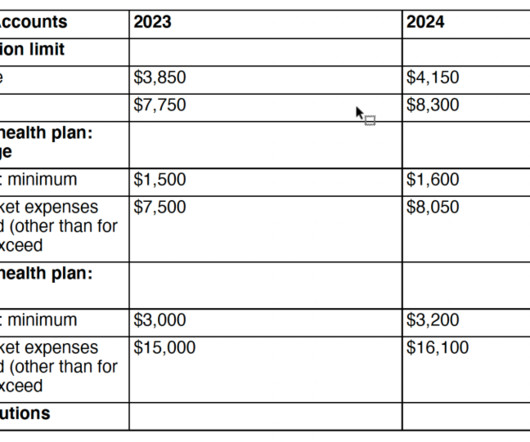

An HSA is a tax-advantaged account that enables you to save money to cover health-care and medical costs that your insurance doesn’t pay. Withdrawals used to pay qualified medical expenses are free from federal income tax. Here are the updated key tax numbers relating to HSAs for 2023 and 2024.

2 Often, this is the first time that many Baby Boomers realize that decisions around Medicare aren’t just medical decisions; Medicare decisions also have significant financial implications. If they start their online application and receive a re-entry number, they can go back to Social Security to finish their application at a later time.);

Keep the following documents for seven or more years: Income tax returns (federal and state) W-2s and 1099s Medical bills Contracts Receipts for tax-deductible items Mileage records Canceled checks Real estate tax forms Credit cards statements that contain purchases used as tax deductions Retirement plan contributions.

4 The caregiver might not be able to work outside the home for enough hours per week to qualify for retirement benefits. She may not be able to remain in the workforce for an adequate number of years to help fund her own retirement, and caregivers may be called upon to help pay for medical supplies or food.

Retirement Planning 5 Reasons Why Houston Is a Great Place to Retire Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. For many people, retirement offers the time and opportunity to travel and explore new endeavors they never had the time for during their working years. Is Houston a good place to retire?

Throughout March, Nationwide is highlighting the unique perspectives of women investors, particularly those approaching retirement, and the opportunities for financial professionals to support their financial goals. Women are more in control of their finances than ever. trillion in annual revenues.

RETIREMENT 3 Retirement Mistakes to Avoid Schedule a Complimentary Financial Review CLICK HERE TO SCHEDULE. Your retirement years can be spent focusing on your family and friends, traveling to places you’ve always wanted to go with your partner, and continuing the hobbies you love at home. Part B: Medical insurance.

Those numbers make it clear that farmers are generally not retiring at age 65. Yet even though many farmers lack a “plan” for retirement in the traditional sense, farmers still need the help of financial professionals. Retirement Income and Transition Planning in Agriculture. Social Security for Farmers.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content