June

20

June

20

Tags

You can’t handle the truth – Do the Math on the 2023 Bull Market

By David Nelson, CFA

The narrative for 2023 and a bull market that continues to get little respect is that without the support of its $trillion market cap members, most of the market is little more than roadkill. Apple (AAPL), Microsoft (MSFT), Alphabet (GOOGL), Amazon (AMZN) and its latest addition, Nvidia (NVDA) have put in a spectacular first half with some believing as soon as they weaken, markets will head south, possibly retesting the lows of last year.

Bloomberg Data

Is that true? Or is something going on here that investors need to know and understand? Let’s find out.

Nothing sells news better than a hurricane

The broadcast and print media will continue to pump this story right up until the time clicks and views start dying off. Nothing sells news better than a hurricane. The pain and destruction from last year’s bear market rivals that of a Category 5 storm

Who can blame them?

Bloomberg Data

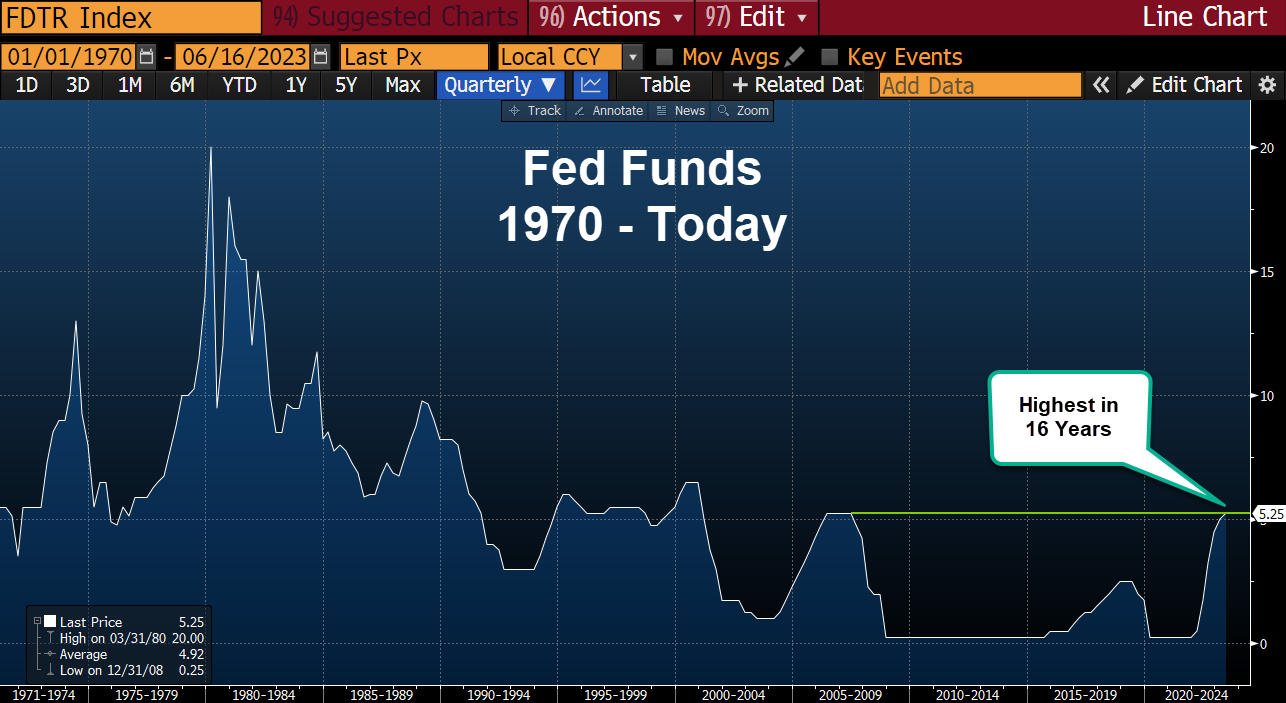

$Trillions were lost, with many fleeing to the safety of Treasuries and CDs as a safe port in a raging storm. Who could blame them? 5% yields are an attractive alternative to risk assets, especially since it’s been close to 16 years since overnight rates were at current levels. While the S&P 500 hit bull market status earlier this month and is now up double digits year to date, much has been made of the fact that the equal weighted index is up only 5%.

Bloomberg Data

What isn’t being reported is that the equal weighted index hit bull market status in February, a full four months earlier.

Equal Weighted Index in a Bull Market?

Bloomberg Data

Off the bottom of last October and start of the year, the tide lifted all boats. However, the banking crisis that followed in March was a heavy burden for stocks as fears of systemic collapse continued to feed the bear market narrative. With close to 14% of the equal weighted index in financials and the fact that smaller banks were hit hardest, the damage was just that much more severe.

Average financial stock dumped 22%

Bloomberg Data

The average financial stock dumped a quick 22%. Fears mounted that Fed policy would continue to force mark to market losses when banks sold held to maturity fixed income to meet deposit outflows. Even with that as a continued threat, evidence continues to mount that an ever-rising number of companies are starting to participate in the most hated bull market of my career.

Do the Math

Let’s do the math. Bears say all of the focus is on the biggest companies with little attention being paid to the smaller, more challenged stocks, which are a better barometer of market health. Okay, let’s go there. What better index than the Russell 3000, which includes the Russell 1000 big cap universe and the Russell 2000 small cap index.

How many companies in the Russell 3000 are up YTD?

1597 / 2903 = 55%

Bloomberg Data

It’s interesting that there are only 2903 securities in the Russell 3000, but it’s still a pretty healthy representation of corporate America. So how many of those companies are up year to date? Better than half coming in at 1597 or 55%.

How many are up more than 15% this year. 908 out of 2903 or 31%, almost one third match the return of the S&P 500, which we know is dominated by large cap secular growth giants. In fact, more than 500 stocks in the index are up more than 30% year to date.

908 / 2903 = 31%

Bloomberg Data

I know what you’re thinking. It’s all about artificial intelligence and technology stocks and without the help of a bubble, the numbers would be toast. Let’s take a look. When technology stocks are stripped out, we now have a universe of 2479 stocks. We still end up with 777 or close to one third in bull market status, up greater than 20% off the October lows.

Nvidia (NVDA) doesn’t even even make the top 10

Bloomberg Data

Even with technology put back in, the percentages only improve by 2%. Year to date, NVIDIA doesn’t even make the top ten in performance, all of which are up over 200%. The point is the bear thesis of narrow participation in the bull market just isn’t holding water.

Are there risks? You bet. But there are even more opportunities. A.I. and other exciting technologies are just the beginning.

Will A.I. turn into a bubble? Of course, it will. Investors can’t help themselves, but I still stand by my call that we’re in the early innings. The current landscape looks a lot more like 1996 than it does 1999. The internet bubble still had years to run. The fact that so many companies are being forced to introduce an A.I. initiative only speaks to the power of the technology.

Board directors will force management’s hand or push for changes at the top if they don’t come up with a way to use A.I. and or large language models to drive better performance. The good news is that report cards are likely at least a year away. Few will expect results from a company like Campbell’s Soup, which recently announced their artificial intelligence rollout to better identify product and consumer trends. A year from now, investors will want to see that strategy bear fruit, but for now will focus on the core business.

Bloomberg Data

The companies that have to deliver today, are the same names that drove the early part of this bull market. Nvidia, Microsoft, Alphabet, and others at the heart of A.I. will need to continue to drive revenue, cash flow and earnings sequentially with little room for disappointment.

All the usual suspects

The risks? All the usual suspects. If the current bull market is going to end, it will likely be the result of one of the following. The Fed and its history of policy errors looms large for investors. No question the challenge is real. They’ve already buried a few banks and continued hikes will add to pressures building in our financial infrastructure.

China is still the biggest risk

Half a world away, China increasingly becomes a risk to market stability. The failure of its post zero-covid policy is there for all to see. China’s central bank cut rates last week in an effort to jump start its failing economy. With youth unemployment at record highs and an economy losing steam, Beijing is even considering unwinding policy that helped clamp down on excessive speculation in its property markets. While the world continues to decouple from China, it is still the world’s second largest economy and a key factor to global growth. Every corner of the planet is a geopolitical hot spot and will continue to be a tail risk that’s difficult to quantify.

I’ll leave you with the following and a repeat from my post last week. There does come a time in every market cycle where market emotions cross. The first Fed hike in this cycle came in March of last year and ushered in an emotional shift with fear resonate in the hearts and minds of investors.

Returns are relative. A risk-free rate of better than 5% is an extremely attractive return, especially with some of the headwinds that will likely be with us for some time. However, each stair step higher in market return will challenge that thesis as investor emotions swing from fear to greed.

*At the time of this article some funds managed by David were long AAPL, MSFT, GOOGL, AMZN & NVDA