This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

trillion annually over the next decade as part of the great wealth transfer, a new report finds. trillion annually over the next decade as part of the great wealth transfer, a new report finds. trillion annually over the next decade as part of the great wealth transfer, a new report finds.

At The Money: The Right Way to Spend Your Money in Retirement (July 16, 2025) One of the biggest challenges of retirement is actually spending your money! After decades of working, saving, and investing, pivoting to spending down your accumulated wealth can be surprisingly difficult.

Podcasts Christine Benz and Amy Arnott talk the state of retirement with Anne Tergensen of the WSJ. morningstar.com) Barry Ritholtz talks shareholder yield with Meb Faber of Cambria Investments. podcasts.apple.com) Taxes A year-end taxplanning checklist. humbledollar.com) How to retire without regrets.

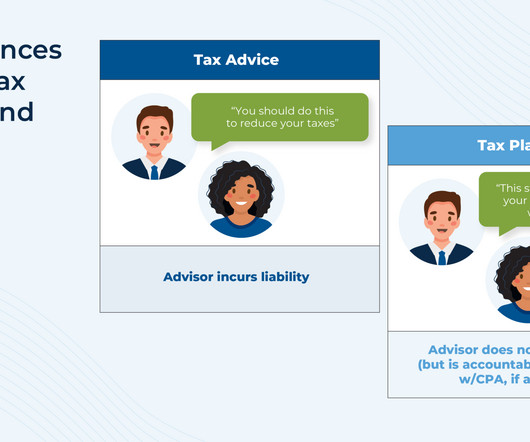

In recent years, financial advisors have increasingly embraced taxplanning as a core element of delivering value to clients. Despite this growing interest in tax conversations, most advisors are still quick to distinguish their services as "taxplanning", not "tax advice" – a distinction largely driven by liability concerns.

Also in industry news this week: NASAA has proposed an amendment to its broker-dealer conduct model rule that would restrict the use of the terms “advisor” and “adviser” for broker-dealers and their registered representatives who are not also investment advisers or investment adviser representatives A recent study suggests that (..)

What's unique about Daniel, though, is how his firm has expanded its tax focus to include "in-house" tax return preparation for its clients as a one-stop shop, but actually outsources the tax preparation work itself to trusted CPAs that he pays out of his own revenue (rather than bringing this service fully in-house) so that he can focus his staff (..)

Enjoy the current installment of "Weekend Reading For Financial Planners" - this week's edition kicks off with the news that SIFMA, which represents broker-dealers, investment banks, and asset managers, released a white paper that argues that CFP Board "increasingly functions as a de facto private regulator for CFP certificants" and proposes that CFP (..)

As the year comes to a close, now is the time to review potential financial moves to help minimize your tax burden heading into 2025. Proactive year-end taxplanning can lead to significant savings and set you up for financial success in the new year. GET STARTED 1. For those over 50, the limit is $8,000.

based accounting firm, is taking a page from large registered investment advisors by bringing together taxes and wealth management. Minopoli, who is also a partner in the new RIA, had previously been the chief investment officer of a team managing a $30 billion portfolio for the Knights of Columbus Asset Advisors.

RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth RIA Edge Podcast: Schwab’s Jalina Kerr on How Resilient RIAs Can Turn Market Volatility Into Growth Jalina Kerr of Charles Schwab shares how the most adaptive firms are expanding beyond portfolio management, into areas like estate and taxplanning.

If you are someone who loves a good Do It Yourself (DIY) challenge, whether it is fixing your own car or kitchen sink, you might think investing is just another task you can master on your own. Self-investing, or DIY investing, is incredibly popular. What is self-investing, and what are its pros and cons?

As December unfolds, it’s easy to overlook year-end taxplanning amid the holiday hustle. However, dedicating a few moments now can lead to significant savings come tax season. To help you retain more of your hard-earned money and reduce your tax liability, consider these five strategic moves before the year concludes.

Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B Resonant Capital Merges with Tax, Accounting Firm QBCo $2.2B Resonant Capital Merges with Tax, Accounting Firm QBCo Wisconsin-based Resonant Capital and QBCo will share clients across wealth and tax in an increasingly popular service model. based QBCo Advisory.

Alternative investments such as private equity, cryptocurrencies, and collectibles now represent a significant part of the investment arena, in particular to high-income individuals. Table of Contents What are alternative investments? What are the key tax strategies for alternative investments in 2025?

Interest rates remain a significant factor in financial planning, affecting everything from mortgage rates to investment returns. The Foundation: Emergency Funds and Debt Management The cornerstone of any solid financial plan is having a robust emergency fund. This can significantly impact your retirement savings trajectory.

At Zoe Financial, we’ve seen firsthand how proactive planning with a fiduciary advisor helps individuals protect and grow their wealth across generations. This guide consolidates what we’ve learned to help you refine, update, or pressure-test your current retirement and estate strategy with confidence.

While a Roth conversion may never make sense for some individuals, for others, early retirement years may be the best time to convert pre-tax accounts to tax-free Roth. Your current and projected future tax rate is often a main component of the decision, but there are other considerations and benefits as well.

Life transitions such as marriage, divorce, the birth of a child or grandchild, career changes, retirement, an inheritance, or the purchase or sale of a home can all influence your broader financial picture. These events may affect your investment approach, taxplanning strategies, insurance needs, and estate planning documents.

Items costing less than $2,500 can typically be expensed immediately, while more substantial investments may require depreciation over time according to IRS guidelines. These variables can significantly impact the final deduction amount, necessitating strategic planning to optimize this benefit.

In this comprehensive guide, we’ll explore proven strategies to help you minimize tax liability while staying compliant with current regulations. From maximizing deductions to managing capital gains, we’ll cover everything you need to know about smart taxplanning.

While you are busy earning, investing, and scaling your income, it is easy to overlook the importance of protecting what you have already built. With the right high-net-worth investing strategies, you can keep your wealth intact without turning your life upside down. Making sure it lasts, not just your lifetime but also after you.

In this article, well examine the most effective end-of-year tax strategies to help maximize your deductions and reduce your taxable income. These contributions not only provide immediate tax relief but help secure longer-term financial stability during retirement.

Employee Stock Ownership Plans (ESOPs) An ESOP allows owners to gradually sell their shares to employees through a qualified retirementplan. This can be an effective way to preserve company culture, reward loyal staff, and capitalize on significant tax benefits.

The ability to deduct the full fair market value of contributed long-term appreciated assets creates substantial tax savings for professionals looking to optimize their tax situation. DAFs also introduce welcome simplification at tax time by consolidating multiple charitable activities under a single receipt.

Unexpected events can derail your progress toward your goals and even your financial security if you don’t have a plan for managing them. Financial planning should ideally involve every area of your financial life because they are all interrelated. This is one of the fundamental principles of investment risk management.

Backdoor strategies are retirement contribution methods that allow individuals to bypass income limits and contribute to tax-advantaged retirement accounts. The strategies typically involve making after-tax contributions to a traditional IRA or 401(k), then converting those funds into a Roth IRA or Roth 401(k).

In this article, we’ll break down the concept of waterfall wealth distribution, its benefits, and how it compares to traditional investment strategies. We’ll also explore the role of income tiers, provide real-world case studies, and highlight key considerations when implementing this strategy in your financial plan.

In today’s dynamic economy, millions have embraced a diverse portfolio of income streamsfrom traditional employment to creative side hustles, equity compensation, and investment ventures. This makes income classification a crucial factor in taxplanning, loss utilization strategies, and overall financial health.

Let’s be honest, retirement isn’t what it used to be. The traditional blueprint of working until 65, collecting a pension, and retiring feels outdated, especially for mid-level professionals who’ve started thinking early about what their ideal retirement should look like. Start planning early. And the best way to do that?

Every year brings changes in tax rules, and 2025 is no exception. Whether you are saving for retirement, running a business, or planning for your family’s future, these updates could affect your financial decisions throughout the year. Think of it as the tax system’s way of protecting your purchasing power.

As Doug Waite of LexTax explains, “Whether to take itemized or standard deduction all depends on if your itemized deductions (medical, state and local taxes, mortgage and investment interest expense, charitable contributions, and certain miscellaneous expenses) exceed your standard deduction.” Why do tax credits exist?

Rising incomes, complex tax rules, countless investment options, and growing aspirations have made personal finance decisions more challenging than ever. Here’s the pathway under the current education structure: InvestmentPlanning Specialist – Focuses on asset classes, portfolio strategies, and wealth accumulation.

Lothes focuses on estate planning for high net worth individuals including estate, gift and generation-skipping transfer taxplanning, will and trust preparation, estate and trust administration, and charitable giving. Lothes is a partner at Gilmore, Rees & Carlson, P.C., located in Wellesley, Massachusetts.

Running focused social media campaigns that highlight their services and share their skills in areas like taxplanning or retirementplanning. Registered Investment Advisers (RIAs) have to follow several SEC rules. This is very important when you discuss investment results or share testimonials.

While most taxpayers dont need to worry about estate and gift taxes, having significant assets can make them a challenge. Also, like most UHNW individuals, you may have income from several sources like investments, real estate, and business interests that may require special taxplanning. Donate to qualified charities.

A financial plan looks at your assets and liabilities, short-term and long-term needs, as well as your goals to structure your finances in a way that suits you. Want to retire early? Financial planning shatters many allusions you might have about how money works. TaxPlanning. Emotional Investment Choices.

Private equity and alternative investments create unique tax reporting complexities that demand attention. Inside these investment structures, K-1 and 1099 forms represent fundamentally different approaches to reporting income and losses, each with its own set of rules and implications.

Whether clients support the policies with cash gifts or split-dollar, the discussion of options will necessarily involve a combination of insurance planning, taxplanning, income and gift tax-oriented wealth transfer planning and investmentplanning.

Let us face ittech startups encounter a unique set of tax challenges that can make or break their financial future. The complex interplay between traditional tax regulations and the innovative nature of tech businesses demands smart planning from day one.

Tax-loss harvesting is a powerful strategy that investors can use to reduce their taxable income. This type of strategy typically involves selling underperforming investments at a loss to offset capital gains (or ordinary income) to optimize portfolio returns. Is tax-loss harvesting right for you?

A good rule of thumb is to set aside at least 30% of every payment you receive to cover your estimated tax obligationshowever, this percentage may need to be adjusted based on your individual tax bracket. On the whole, its advisable to consult a tax adviso r to develop a dependable taxplan.

Roth IRA conversions present a significant challenge for retirement planners: pay taxes now or later? Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. One of the Roth IRA’s most compelling features?

Event Invitation Follow-up “Hi [Client Name], thanks for your interest in our retirementplanning workshop. New Service Introduction “Hi [Client Name], we’re now offering taxplanning services that could save you significantly next year. How do advisors track return on investment?

The key benefits Reduced tax liability: So long as youre paying reasonable wages to your child, you can lower overall tax liability. For instance, children can earn a gross income up to $14,000 (2024) tax-free under the standard deduction, shifting income to a lower tax bracket. General Risks Relating to Digital Assets.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content