Tuesdays are all about academic (and practitioner) literature at Abnormal Returns. You can check out last week’s edition including a look at the poor performance of retail option traders.

Quote of the Day

"Whatever the reason, the existence of some persistent investment factors is today accepted by most (if not all) financial economists and investors. The approach might not be perfect — like all attempts to impose a scientific framework on human weirdness — but it is a useful prism through which to look at markets."

(Robin Wigglesworth)

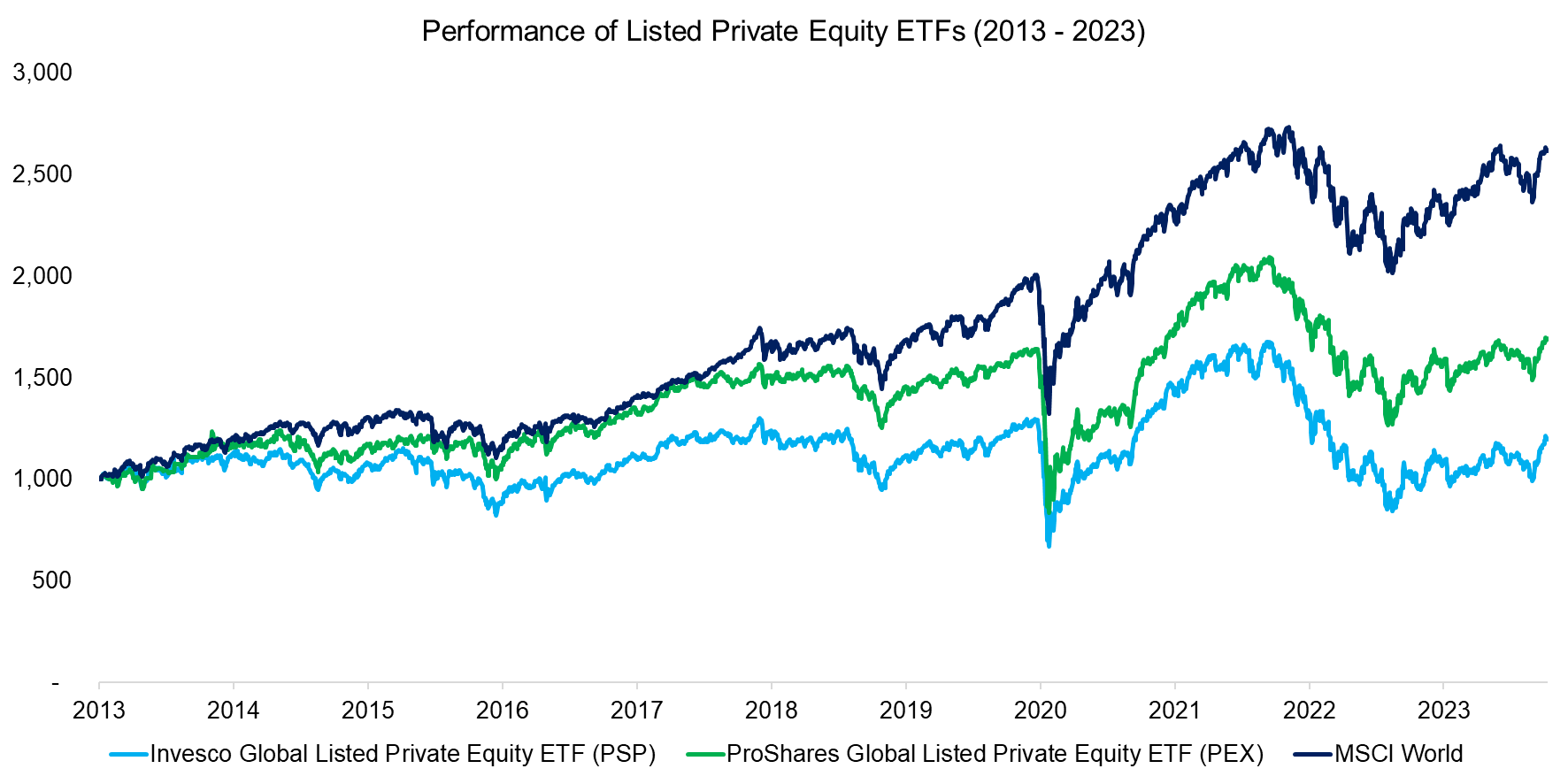

Chart of the Day

The returns to publicly traded private equity have been dismal.

Factors

- Timing returns factors is tempting, but difficult in practice. (alphaarchitect.com)

- The high quality anomaly shows up across asset classes. (advisorperspectives.com)

- A history of quant investing and the state of the factor zoo. (on.ft.com)

Corporate finance

- Stock-based compensation makes a big difference for company valuations. (tdmgrowthpartners.com)

- Profit margins are high, debt refinancings are coming. (canvas.osam.com)

- Family firms do a better job of keeping information secret. (papers.ssrn.com)

Research

- What would it take to see a repeat of U.S. equity performance in the next decade? (aqr.com)

- Why it's so hard to make money betting against the stock market. (klementoninvesting.substack.com)

- Historical performance doesn't really help pick outperforming managers. (indexologyblog.com)

- Inflation makes tax efficiency all the more important. (aqr.com)

- Reinsurance returns are not surprisingly uncorrelated with traditional asset classes. (advisorperspectives.com)

- Can you use alternative measures to invest across countries? (quantpedia.com)

- Retail attention is a mixed blessing for stocks. (papers.ssrn.com)

- Star analysts hit the road. (papers.ssrn.com)