July

31

July

31

Tags

Every Bull Market has an Achilles Heel

By David Nelson, CFA CMT

This is what most investors see when they look at a chart of U.S. stocks.

Bloomberg Data

This is what I see.

Bloomberg Data

Stocks are just 5% from an all-time high and a ball spiking end zone dance. The sentiment has turned bullish but making it across that goal line won’t be a walk in the park. Just like in football, the last few yards in the Red Zone can be the toughest.

On Thursday last week, we saw how fragile that sentiment is. Every bull market has its Achilles heel and this one is no different.

Welcome to the Money Runner. I’m David Nelson.

Every time ten-year Treasury yields start to approach 4%, investors get nervous and start taking down exposure. That’s exactly what we saw Thursday last week. I didn’t notice it right away, and maybe you didn’t either, but the computers did. One by one they started kicking off sell programs, wiping out the day’s gains.

Bloomberg Data

Look at 30-minute bar charts for the S&P 500, up against ten-year yields. Once there’s even a hint that ten-year rates are heading above 4%, the sell programs kick in. The reversal was notable in that Thursday was a risk-on day. Traders and investors were celebrating another breakout performance from Meta (META) now up 175% year to date.

Bloomberg Data

This time it wasn’t comments from a rogue Fed official or even a hot economic release that ended the party. No, this time the trigger was pulled half a world away. The Bank of Japan loosened its policy of managing the yield of ten-year Japanese government bonds. The BOJ already owns more than 50% of all outstanding JGBs.

That shift likely caught world debt markets off guard, forcing fixed income and equity traders to adjust. I think this setup hurt hedge funds on Friday.

Bloomberg Data

On Thursday, hedge fund managers pressed their short book heading into the close, looking to cash in on the heels of what market technicians call an outside day. Traders added to their shorts confident in a Friday payoff.

What is an Outside Day?

Outside days are often a sign of increased volatility and a possible reversal in the prevailing trend.

- The current day’s price bar has a higher high and a lower low than the prior bar.

- The open and close of the second day fall outside the open and/or close of the first day.

- The outside day occurs during a period of trending market conditions.

- Outside days are often accompanied by increased volume.

Unfortunately for the Bears, any hope of cashing in those chips on Friday melted away once the inflation numbers started rolling in. The economic releases were in line or better than expected, showing once again what stocks had sniffed out months ago.

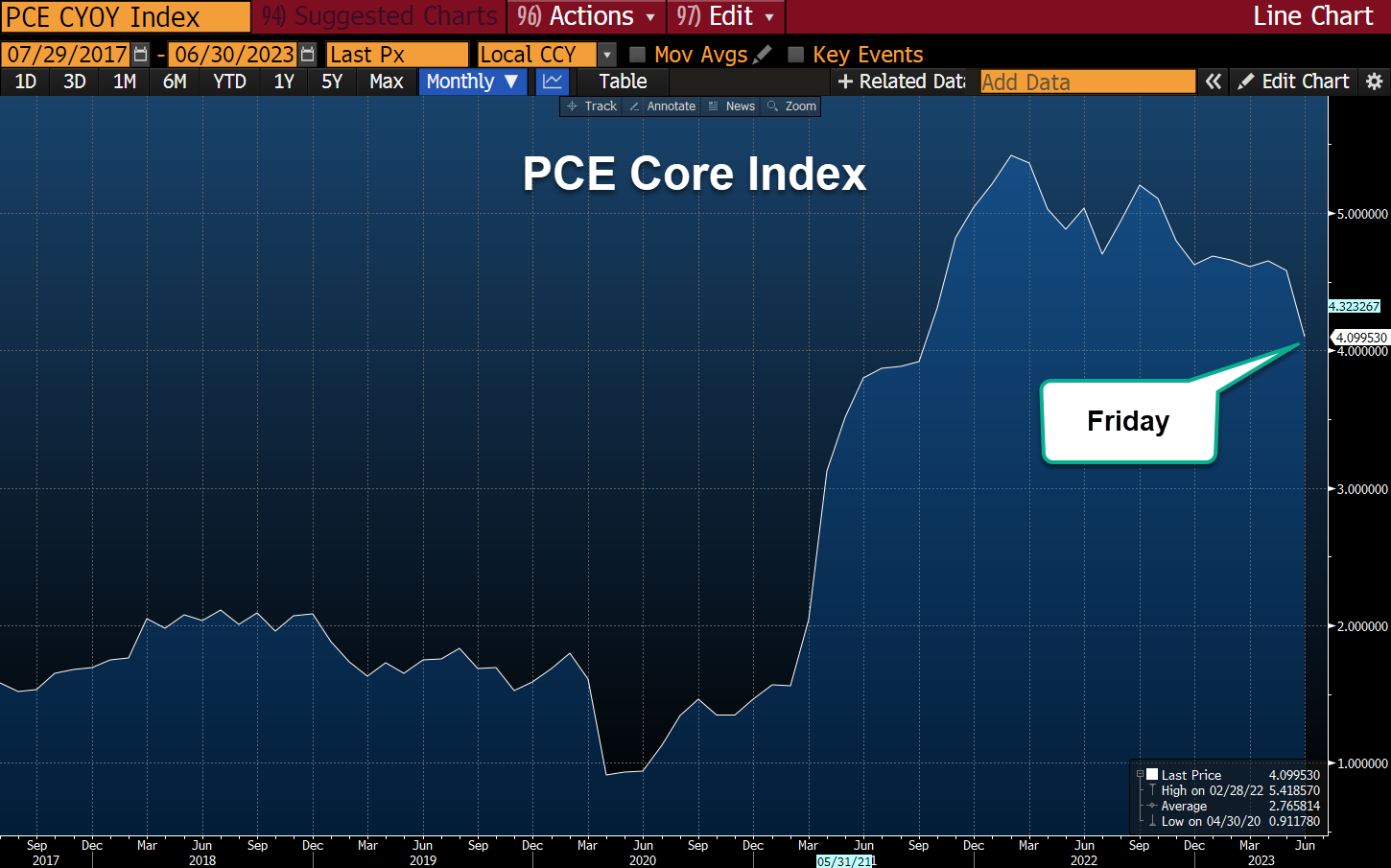

The Fed’s favorite indicator, PCE Core Index came in as expected and decidedly on a downward trend.

Bloomberg Data

The Employment Cost Index came in a full 10th of a percent better than advertised and now sits at 4.5% year on year.

Bloomberg Data

Inflation continues to head south, suggesting the Fed is done or at worst very close to peak Fed Funds. We can debate higher for longer or even the wisdom of a Fed cut, but what isn’t up for debate is that the US economy has bigger concerns than a hawkish Federal Reserve.

The Fed has done their job. It’s time for government to do theirs. End blank check politics designed to buy votes while catering to the will of lobbyists and big donors.

Bank of Japan

The policy shift from the Bank of Japan caught most of the street off guard. We have a myopic focus on inflation, the Fed and the Magnificent Seven stocks that have driven much of the market performance this year. We forget that forces beyond our borders can have an outsized effect on markets here.

Are there risks out there? You bet. But there are even more opportunities. We’re not in crisis mode anymore. The bear market low was last October, a view that is rapidly becoming consensus.

That shift in sentiment provides needed support for markets. The mountain of cash and cash equivalents sitting on the sidelines is fuel ready to be deployed. We’ll have corrections along the way, but now those corrections will be viewed as an opportunity rather than a liability.

Earnings on Deck

On deck this week, we have two more of the Magnificent Seven stocks reporting. Apple (AAPL) and Amazon (AMZN) report Thursday evening, setting up for a monster trading day on Friday. Why? Not only will we have two very important earnings reports driving market action, but we also get July jobs numbers that will in part influence the Fed’s next rate decision.

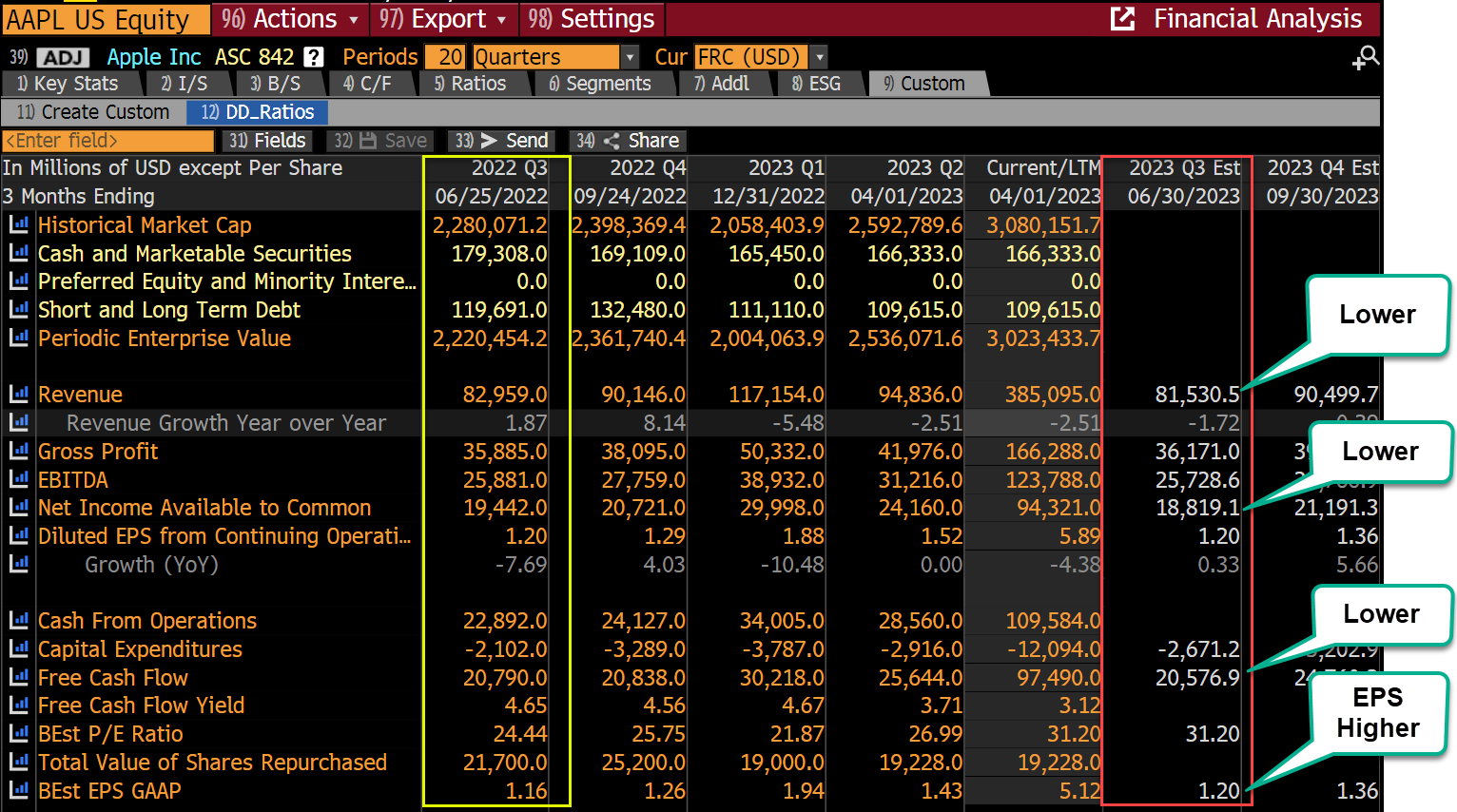

Apple is clearly the toughest to defend, given that just about every line item on the income statement will be down year on year.

Bloomberg Data

Take your pick, Revenue, Net income, Free Cash Flow? All will be lower than this time last year. The only line item that will likely improve is earnings per share as Tim Cook continues to buy back stock. Remember, a stock buyback does nothing for revenue or net income. It only inflates EPS because the share count goes down.

We learned long ago that valuation is not the only data point that drives equity prices. If that were true, Apple (AAPL) would be trading at 100 instead of waltzing into this report, close to 200. The mystique that surrounds Apple has helped support a market cap rapidly approaching $3 trillion. Add a massive installed base of users and a 30% cut of every purchase in the App Store, it becomes hard to argue with their success.

If the market has an Achilles heel, the App Store and that 30% share is Apple’s. Regulatory risk is the biggest challenge for CEO Tim Cook along with every shareholder.

Amazon

Amazon (AMZN) is another company where investors have chosen to look beyond valuation. Bulls on Amazon will be looking for strong commentary on AWS growth in the second half this year, as well as improved margins at retail. Also look for comments on generative A.I. and how they intend to harness its power. Part of the bull thesis is an expected ramp up in AWS services as demand from this secular growth story kicks into gear.

At 50x 2023 earnings, there isn’t much in the way of valuation support. Of course, at Amazon there never was.

*At the time of this post some funds managed by David were long AAPL, AMZN & META