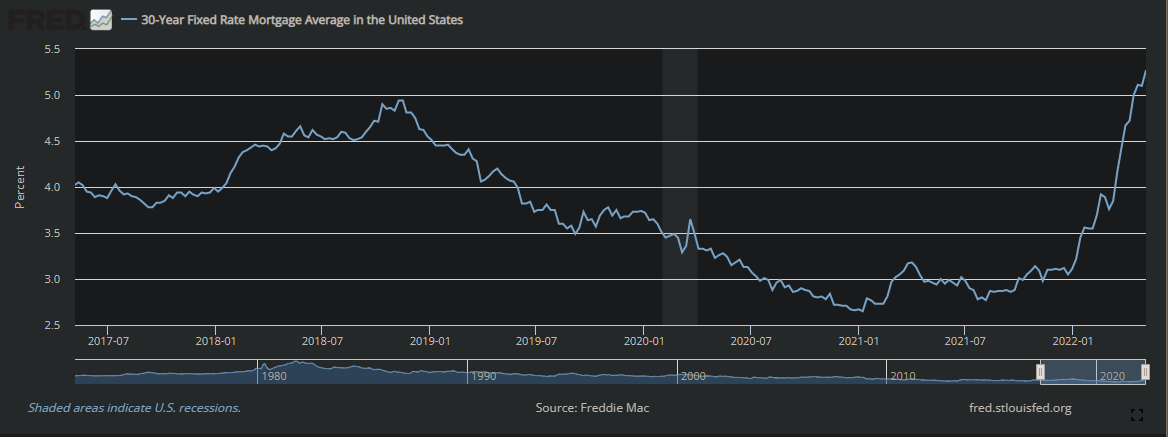

Image Credit: Aleph Blog with help from FRED || Look at the mortgage rates fly!

Okay, you might or might not remember the last piece. But since that time, 30-year mortgage rates have risen more than 1%. Is the Fed dawdling? Maybe, but the greater threat is that they become too aggressive, and blow up the financial economy, leading us into another decade-long bout of financial repression.

As it stands right now, mortgage rates are in a self-reinforcing rising cycle, and it will not end until the Fed raises the Fed funds rate until it inverts the Treasury yield curve. But if I were on the FOMC, I would ignore inflation and the labor markets, and I would watch the financial economy to avoid blowing things up.

The FOMC won’t do this. They are wedded to ideas that no longer work, or may never have worked, like the Phillips Curve. They imagine that the macroeconomic models work, when they never do. They forget what Milton Friedman taught — that monetary policy works with long and variable lags. Instead, in tightening cycles, the FOMC acts as if there are no lags. And, in one sense, they are correct. The financial economy reacts immediately to FOMC actions. The real economy, with inflation and unemployment, may take one or two years to see the effects.

And because the FOMC forgets about the lags, they overshoot. The FOMC, far from stabilizing the economy, tends to destabilize it. We would be better off running a gold standard, and regulating the banks tightly for solvency. Remember, gold was never the problem — bad bank regulation was the problem.

=======================

One more thing — the Fed needs to be quiet. The chatter of Fed governors upsets the markets, as do Fed press conferences and the dot-plot. The Fed was most effective under Volcker and Martin. They said little, and let their actions be known through the Fed’s Open Markets Desk. That allowed the Fed to surprise and lead the markets. The current Fed (since Greenspan) made the mistake of following the markets. Following the markets exacerbates volatility, and promotes oversupplying liquidity.

=======================

At present I am pretty sure 30-year mortgage rates will rise to 6%, and maybe 7%. No one is panicking enough on this, so it will likely go higher. MBS hedging is a powerful force, and will continue until people no longer want to buy houses at such high interest rates.

1994- For the Fed unemployment mandate, which is perhaps the most important variable, unemployment was stable to decreasing, so that’s a success.

Gold Standard- The economic history under the gold standard was not some kind of utopia. There were several business cycles (including the 1930’s) where the gold standard was an arbitrary and harmful drag on economic activity. Some kind of commodity-index backed currency might be good (Friedman’s idea), because of diversification, etc. Gold-backed currency is not a serious possibility.

Thanks for your work.

Hello there,

Random engineer here. I like you comment on how the Fed lagging the market tends to increase volatility. That fits well with Control Feedback Theory which basically says that the longer the lag between sensor input(market behavior) and the correcting feedback(the Fed), the worse your controller will be. (Aka the Z transform of your system instead of the classical LaPlace Transform). If the lag is bad enough, the whole system may become unstable. Granted, that assumes that one is able to stabilize the system in the first place…