This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

ESG companies focus on a range of things, such as reducing carbon emissions, cutting plastic waste, treating employees fairly, ensuring gender equality, and prioritizing ethical governance. That kind of pressure ensures companies prioritize ESG governance and ethical practices. When it comes to ESG, it is not just about investors.

It is easy to get caught up in growing your wealth, chasing high-net-worth investment opportunities , or expanding your financial portfolio, but wealth preservation deserves just as much of your attention. Securities and Exchange Commission (SEC), the thresholds may vary slightly — say a net worth of $1.5 According to the U.S.

Share important articles, industry news, and useful tips on financialplanning. Always follow the rules for sharing financial information on social media. Understanding Your Client’s Unique Needs Understanding your target market and what your target clients need is important for good financialplanning.

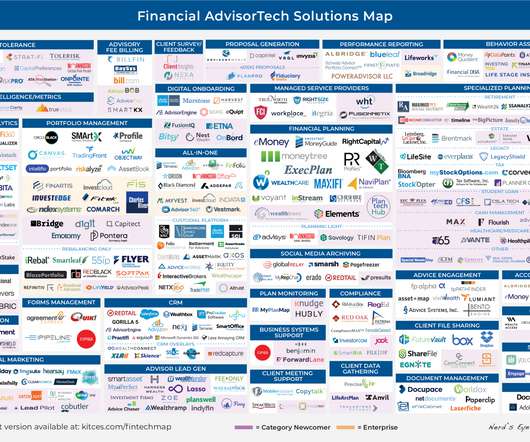

Welcome to the October 2022 issue of the Latest News in Financial #AdvisorTech – where we look at the big news, announcements, and underlying trends and developments that are emerging in the world of technology solutions for financial advisors!

But a lawsuit to block the rule ultimately led to it (and the associated Title Protection for "financial planner") being vacated… by the FPA. even as the CFP Board has announced its own Competency Standards Commission to raise their own standards regarding who can use the Certified Financial Planner title?

In this episode, we talk in-depth about how Carolyn grew her career to become a leader in the financial services industry and made her mark by becoming an established executor for major broker-dealers that wanted to shift away from solely commission-based models and add advisory models, the paths that Carolyn navigated at companies like H.D.

.” Only 4 percent of Certified Financial Planner™ professionals identify as Asian American or Pacific Islander (AAPI), though they make up 6.2 1,2 Despite the small numbers, AAPI professionals remain the largest ethnic minority within the financialplanning profession. percent of the American population.

Ethicalfinancial advisors are on the rise and are now doing things within their businesses with the hope to serve as an example of the right behavior for the rest of the industry to follow. Note: Envision Wealth Planning and James Brewer are featured in #7!*. Ethics matter in financial advice! Ethics matter.

So here’s a blog about some things that ethicalfinancial advisors do in the hopes they will serve as an example of right behavior for the rest of the industry to follow. I am an irreverent and fun marketing consultant for financial advisors. Ethics matter in financial advice! Ethics matter.

A Guide for FinancialPlanning When it comes to managing your finances, it’s crucial to work with a professional who puts your interests first. Furthermore, fee-only advisors don’t receive any third-party payments, unlike advisors who earn commissions from financial products they sell.

As the move to transparency in financialplanning takes hold, regulations are changing in Colorado and other states. Here’s the triumph of virtue that financialplanning transparency will (FINALLY) bring to planners across the country and the benefits to clients that come along with it. What should financial advisors do?

The primary fee structures are: Fee-only : Advisors only receive payment from their clients for the services they provide, not receiving any commissions or other incentives from product providers. Fee-based : This structure is a blend of fees and commissions. Between $1,000 and $3,000 A comprehensive financialplan could cost $2,000.

Any financial advisor who is registered as an advisor with a regulator has to fill out this form for initial approval by either a state or a Federal (the United States Securities and Exchange Commission) regulator. What if you can’t find the financial advisor’s Form ADV? Are they just providing financialplanning?

These professionals work independently or under the umbrella of financial institutions and are specialized in guiding clients through the intricacies of financialplanning and investments. Their compensation often comes from (1) commissions on transactions based on advice provided or (2) fees for financialplan construction.

Fee-Only financial advisors are most often compensated as a percentage of assets (AUM), though also may be paid hourly, as a retainer, or as a flat fee, depending upon the planner you choose. This can include mutual funds, insurance policies, annuities, and other financial products. Fee-based advisors are where it can get complicated.

Fee-Only financial advisors are most often compensated as a percentage of assets (AUM), though also may be paid hourly, as a retainer, or as a flat fee, depending upon the planner you choose. This can include mutual funds, insurance policies, annuities, and other financial products. What does it mean to be a fiduciary?

A financial advisor is a certified financial planner who is licensed and regulated to take mandate decisions on multiple aspects of financialplanning. They may charge for their services either on a commission basis or hourly rates. First of all, the financial advisor has the expertise to do your research.

Certified Financial Planner (CFP) . One of the best financial advisors available, CFPs earn board certification that represents their intensive training, commitment to observing ethical standards, and dedication to putting clients first. Chartered Financial Analyst (CFA) . What is their approach to financialplanning? .

If you’re as old as Methuselah, like I am, you might remember a pivotal moment in the evolution of the planning profession, when Forbes magazine noticed that brokers, life insurance and tax shelter salespeople were starting to call themselves ‘financial planners.’ Pandemonium!

Additionally, acquiring relevant certifications and qualifications such as a postgraduate degree in finance, chartered financial analyst (CFA) designation, or certified financial planner (CFP) certification can enhance credibility and employability.

Our mission is to provide the residents of (insert geographic area) with financialplanning and investment management services that. Please view my Code of Ethics here (insert hyperlink). We provide financialplanning and investment services for a single monthly fee of $x. Business owner. Unilever employee.

Every advisor will have his or her own approach to investing, financialplanning, and other services. What about ethics? Quality of financialplanning services rendered? Depth of financialplan? Ethical actions that financial advisors take. Impact on the client? Are you kidding me?

The interesting thing about the journalism ‘profession’ (it’s really more of an avocation) is that we aren’t bound by any formal ethical rules or guidelines. They are, in my view, exactly like commissioned salespeople who pretend to be professionals and fiduciaries; what they offer is tainted by conflicts, usually undisclosed, often damaging.

Make sure to share valuable content through your emails, like newsletters, market updates, tips on financialplanning, and invites to webinars or events. Email marketing helps you stay in touch regularly, builds strong client relationships, and shows that you are a trusted source for financial guidance.

All you need are a few tools, a good work ethic, and an entrepreneurial spirit. And sites like Shutterstock allow you to sell and earn a small commission for your photos. When I worked multiple jobs, I would schedule in my calendar my full time job hours, my side hustle hours, plus any time I planned to spend with family, etc.

This plan can include a living trust, a legal document that allows assets to pass to beneficiaries without going through probate court. Financialplanning services can assist with developing a comprehensive estate plan. Living trusts can help avoid the costs and delays associated with probate.

And at, at some point, the people that were running the fi, financialplanning department for creative planning, which was a sister company to an insurance company, there were three guys that were selling disability insurance to physicians in Kansas City. And I think, like we were doing financialplanning without a separate fee.

Financial advisors have many options at their hands to solve it, from financialplanning and investment management services to fixed products such as annuities. Are commissions bad? Are commissions bad? Macchia says that agents would be happy to take even a small commission. Sara’s upshot.

We’ll discuss these questions: The CFP Board has specifically stated that it wants the CFP® mark to be a requirement for anyone who practices financialplanning. The debaters are: Robert Wright, CFP®, a financial consultant with Advocacy Wealth Management. What is your opinion? Robert will be on the “for” team.

Get ready for a ride as we examine it from all angles: regulatory, ethically, intellectually, etc. The debaters include: Robert Wright, CFP®, a financial consultant with Advocacy Wealth Management. John Robinson (“JR”), Founder of FinancialPlanning Hawaii, Inc. Robert will be on the “for” team.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content