August

07

August

07

Tags

Confessions of a Money Runner

By David Nelson, CFA

Everyone approaches life and their job differently. I spend some part of my weekend in reflection, looking back over the previous week, asking myself some tough questions. What did I do right? And more importantly, what did I get wrong? The scale is rarely balanced, but if I’m honest with myself, I can usually identify any problems in the process or execution.

The next part is the most important: Do something about it!

All too often, we waltz into our workweek with little in the way of a plan. I don’t care if you work on Wall Street or Main Street. We live in a competitive world. You have to take any new information and adjust your game if needed.

Make no mistake, the last couple of weeks were important for investors. Ultimately, my concerns may fade, but the enemy has fired a shot across the bow. You’re probably asking yourself, “What is this Money Runner guy talking about?”

Bloomberg Data

For the last 18 months, investors have had a myopic focus on the Fed and what Jay Powell and company were up to. Each stair step higher in Fed funds took another bite out of the market, sending stocks into a well-deserved bear market last year.

The hangover from a money-is-free, liquidity-driven bull market was brutal for stock investors, as the cure was a tough pill to swallow. The Fed hiked rates 11 times in an effort to stamp out inflation, partly caused by reckless monetary and fiscal policy. If the Fed is truly data-dependent, they will look at the current data and understand that much of their work is done.

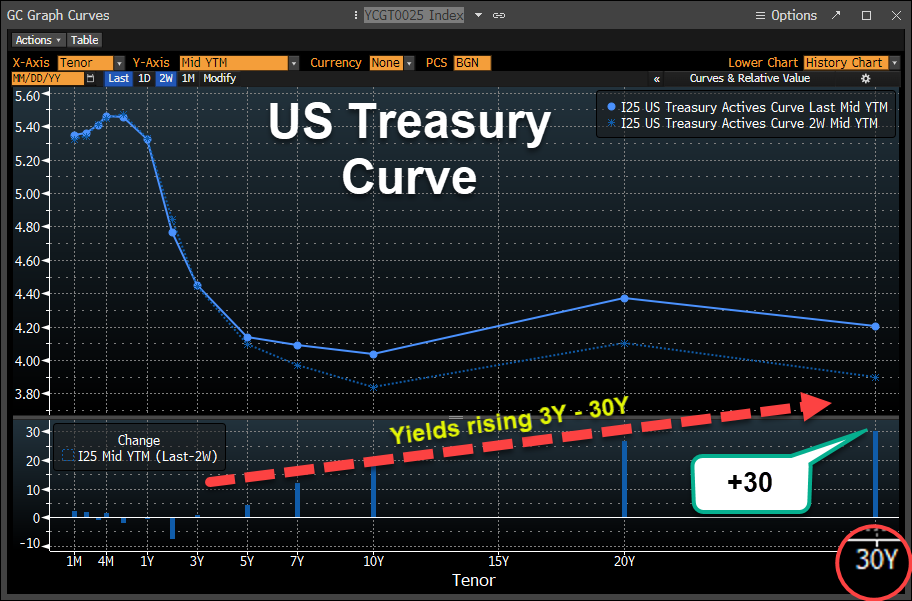

Investors caught off sides

Bloomberg Data

While we were all focused on the front end of the yield curve as an indication of what’s coming next, all the way over on the other side, rates were climbing and climbing quickly. In the last two weeks, from 3 years to 30 years, bonds headed lower, pushing yields higher. The 30-year sparked the most fear, with yields jumping a full 30 basis points.

We’ve had two events in the last couple of weeks that we need to talk about. The first we addressed in last week’s podcast. Every bull market has an Achilles heel. The Bank of Japan loosened the bans around Japanese government bonds, triggering a wave of global debt selling, sending prices down and yields up.

Fitch Downgrade

The second happened last Tuesday when shortly after the close, credit rating agency Fitch downgraded US debt from AAA to AA+. At first, the reaction was a yawn, with stock futures only modestly down that evening. The following day, the selling picked up, with the week ending down by over 2 1/4 percent.

Bloomberg Data

I come at this story looking through the lens of someone who survived the financial crisis. First, Fitch, along with S&P, is the gang that couldn’t shoot straight. This was the firm that completely missed the financial crisis when mortgage debt was clearly not triple-A. They did nothing with their ratings.

Second, they aren’t giving us any new information. I think every American knows that the U.S. prints too much money and that our deficit and debt have ballooned beyond what is rational. Having said that, the downgrade does force us to at least have the conversation and discuss the very large elephant in the room.

Joe Manchin, the senior senator from West Virginia. His comments last week state the obvious. The downgrade “represents a historic failure of leadership by both political parties and the executive branch.”

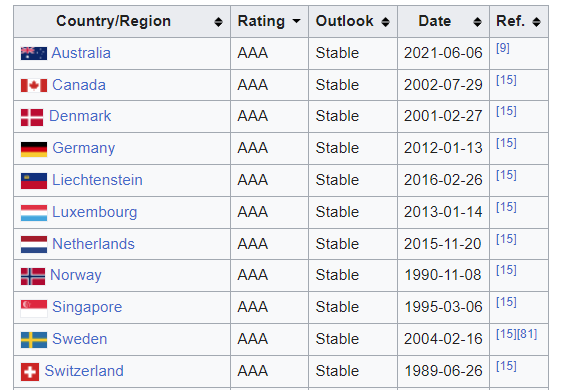

11 other countries now have a better rating than the U.S.

The good news is that we don’t live in a vacuum, and the world is relative. One glance around the planet confirms that the US is unmatched in science and entrepreneurial spirit, the building blocks of any great country. Some will say that there are 11 other countries that now have a better credit rating than the United States. Okay, let’s talk about that.

Six of those countries are members of NATO, with one more, Sweden, waiting to be let in. By definition, they live under the protection of the United States, without which NATO couldn’t function. Keeping your debt in check is a lot easier when you don’t have to fully fund your defense. Having a big brother like the United States ready to step in if a bully threatens does wonders for your budget.

Look at the rest of the list. Does anyone believe that Canada or Liechtenstein is going to challenge the United States as the leader of the free world and the best place for capital?

Nevertheless, the Fitch downgrade is a stark reminder that we can no longer pretend we don’t have a problem. One look across Washington, and the leaders of this great nation don’t inspire a lot of confidence.

If you’re asking yourself how we got here, look at the man or woman in the mirror. We have no one to blame but ourselves. Americans continue to vote in lifetime politicians who understand that the only way they can stay in power is by telling Americans what they want to hear, not what is in the best interests of the nation they serve.

Buffett vs Ackman

The above has sparked something of a debate between legendary investor Warren Buffett and hedge fund rock star Bill Ackman. In an article this weekend, Barron’s discusses Ackman’s short of 30-year U.S. Treasuries, believing that he will cash in as yields climb above 5%. Barron’s goes on to say that Warren Buffett has been adding to three-month and six-month T-bills. That hardly seems like much of a risk. Ackman is the one with the conviction trade here.

Bloomberg Data

For now, investors are going to have to monitor yields at the long end of the curve. I’ve shown this chart for the last couple of weeks, but over the last year, every time ten-year rates poke their head above 4%, stocks start to wobble.

The higher rates keep pressure on market multiples. Just buying the Nasdaq 100 (QQQ) isn’t going to cut it anymore. You’re going to need a rifle, not a shotgun when choosing what to own.

Last week, the debt selling was heavy, pushing up ten-year yields, taking out the June and March highs, setting up for a run at the October highs last year.

On Friday, yields did an about-face, falling in reaction to a benign set of jobs numbers, with some strategists even referring to it as a Goldilocks job market. If you combine Friday’s at 187,000, with last month’s revised downward 185,000, a lot of pressure comes off the Fed, setting up a potential stand pat meeting in September.

The job numbers should have been good news for markets on Friday, especially on the heels of Amazon jumping better than 8%, now up 46% year to date.

AMZN

Bloomberg Data

Amazon beat on just about every line item that matters. E-commerce and AWS were both better than expected. It’s not surprising analysts bumped the average price target to $168, with some sitting north of 200.

AAPL

Bloomberg Data

Unfortunately, the largest company on the planet, Apple (AAPL), rained on that parade with a disappointing quarter, forcing investors to wait for the next product cycle to spark some excitement.

It’s difficult to make a case for Apple based on valuation. As investors, we look past declining sales and net income, holding on to the one metric moving higher: EPS (earnings per share). An endless series of stock buybacks keeps that number steadily moving higher. Apple has the mystique of a must-own stock. There have been many companies throughout history that have played that role. Cisco, IBM, General Electric, all were once stocks we couldn’t afford not to own.

Like I said last week, if stocks traded just on valuation, Apple would be trading at 100. We own it because the price momentum has been up. When a company that represents over 7% of the S&P 500 with a market cap of over $3 trillion marches higher, it’s a stock that’s difficult not to own.

The same is true in reverse. We’ll see how much time it takes for the shares to stabilize. And if my decision to sell 25% of the position will look smart in the weeks ahead.

Fresh Money

Bloomberg Data

A lot of investors are still sitting on the sidelines, looking for an entry point. Now might be a good time to buy into some of the areas of the market that haven’t worked this year.

Look no further than energy. It is the second-worst performing sector but has been quietly rising since late June. Oil is not in the 60s anymore. At close to $83, it is at the highest level since late last year. It’s doubtful that President Biden will release any crude from the SPR, not with it still at dangerously low levels and approaching what could be a difficult hurricane season.

For most companies in the oil patch, earnings are at an inflection point set to rise over the next year. Higher crude prices make it just that much easier.

The service providers like Schlumberger (SLB) and Baker Hughes (BKR) have been the best performers this year, but with crude prices rising, it might be time for the rest of the oil patch to play some catch up.

*At the time of this article, some funds managed by David were long AMZN & AAPL.