This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

based accounting firm, is taking a page from large registered investment advisors by bringing together taxes and wealth management. Minopoli, who is also a partner in the new RIA, had previously been the chief investment officer of a team managing a $30 billion portfolio for the Knights of Columbus Asset Advisors.

If you've heard of a DAF and are curious about incorporating it into your giving and taxplanning strategy, this article is for you. Key Takeaways: Contributions to a donor-advised fund reduce your tax bill in the year your contribution is made. What is a Donor Advised Fund?

Taxplanning serves as the cornerstone of the entire acquisition deal, extending far beyond a simple checkbox. Every element, from structure to price negotiations, hinges on understanding tax implications for all parties involved. Get it right, and you will have set yourself up for a smooth transition and maximized returns.

An 83(i) election is an IRC provision that allows certain employees of private companies who receive RSUs or NSOs to defer federal income tax on the exercise or settlement of their stock for up to 5 years. Before 2017, employees who received RSU or NSO equity compensation faced a dilemma.

Internal Revenue Code (IRC) allows businesses to deduct the full purchase price of certain depreciable assets, including vehicles, in the year of purchase rather than depreciating them over time. Are Capital Gains from Cryptocurrency Tax-Free? General Risks Relating to Digital Assets. Section 179 of the U.S.

Creating wealth that can provide financial security for generations to come is an incredible feat, and it requires careful planning, consideration, and communication among family members. Gifting Other than transferring assets after death, the other primary way to transfer wealth is to gift portions of your estate during your lifetime.

Moving funds from traditional IRAs to Roth accounts triggers immediate taxation but promises tax-free withdrawals in retirement. The stakes became higher after the Tax Cuts and Jobs Act of 2017 eliminated recharacterizationthe ability to reverse conversions that did not work as planned.

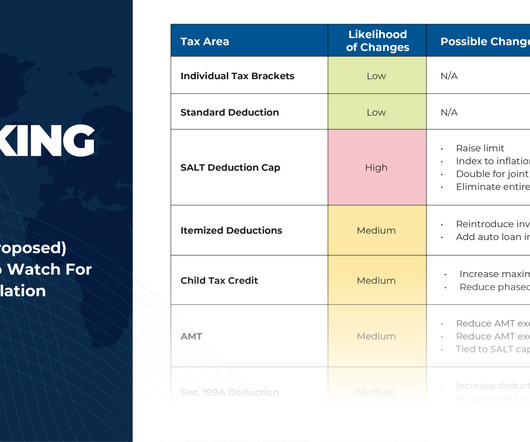

The Tax Cuts and Jobs Act (TCJA)the 2017tax code overhaul designed to boost economic growthis set to expire on December 31, 2025. Unless Congress intervenes, the TCJAs sunset will usher in a swathe of tax increases in 2026, with analysts estimating that over $4 trillion worth of tax hikes could take effect.

Capital gains tax Capital gains tax is what you pay on the profits you earn from selling your capital assets. These include things like stocks, bonds, mutual funds, and other assets. Now, there are two types of capital gains – short-term and long-term, and they are taxed differently.

Harness makes it easy to find tax and financial advisors best suited to your needs. GET STARTED What are the capital gains tax changes in 2025? For individuals with investments in assets such as stocks, real estate, and other securities, changes in the capital gains taxespecially long-term capital gainswill be particularly relevant.

Furthermore, the Trump campaign has proposed a number of additional tax cuts, including tax-free treatment of income from tips, overtime pay, and Social Security benefits, and even eliminating income tax entirely in favor of tariffs. Read More.

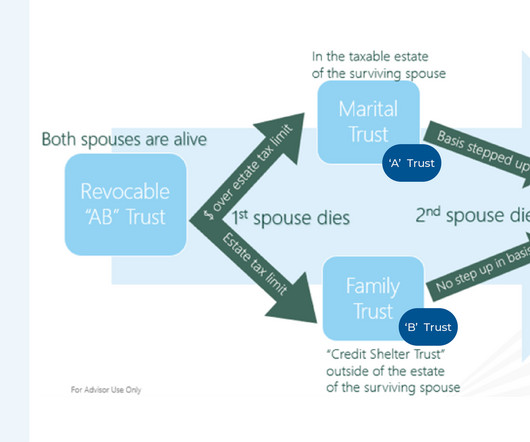

Given how frequently the tax code changes, advisors can add value for clients by ensuring their estate plans are aligned with current law to meet the clients’ objectives, and not with past rules that may no longer apply to them. However, the passage of TCJA resulted in the estate gift tax exemption nearly doubling (from $5.6M

2017 Year-End Planning Letter. Mon, 12/04/2017 - 13:10. presidential election, we have grappled with the lack of clarity regarding the details of new tax legislation. The outcome of the tax reform debate is likely to impact how we advise clients on taxplanning, estate planning and a host of other topics.

The 2017Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

Part 3: Tax-Wise Financial Planning In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. But taxplanning isn’t just for your investments. But we can weave each event into the tax-planning fabric of your financial life.

Part 3: Tax-Wise Financial Planning. In our last two pieces, we covered some tools of the tax-planning trade, as well as how to deploy them for tax-efficient investing. . But taxplanning isn’t just for your investments. Each can translate into tax-planning challenges and opportunities: .

The 2017Tax Cuts and Jobs Act (TCJA) brought sweeping changes to the tax code, impacting every taxpayer and business owner. At that point, many provisions will revert to 2017 levels, adjusted for inflation. For example, in 2017, the marginal tax brackets were 10%, 15%, 25%, 28%, 33%, 25%, and 39.6%.

Starting in 2024, individuals who left assets in a Roth employer plan won’t be subject to mandatory distributions during their life. As with any financial decision, there are pros and cons to leaving money in an employer plan vs rolling it over. is just another massive change in tax law in the last few years.

Whether you are starting a new business or evaluating your current structure, gaining a clear understanding of C Corp taxation will help you make informed decisions and optimize your tax strategy. This means the corporation files its own tax return and pays taxes on its profits at the corporate tax rate.

The Tax Cuts and Jobs Act (TCJA)the 2017tax code overhaul designed to boost economic growthis set to expire on December 31, 2025. Unless Congress intervenes, the TCJAs sunset will usher in a swathe of tax increases in 2026, with analysts estimating that over $4 trillion worth of tax hikes could take effect.

Donors who contribute to a DAF can deposit cash, securities, or other assets into the fund. The donor relinquishes ownership of the assets but retains advisory privileges over how the contributions are invested and how grants are distributed to charities.

For example, as reported by Dimensional Fund Advisors, $1 invested in the S&P 500 Index from 1926–2017 would have grown to $533 worth of purchasing power by the end of 2017, after adjusting for Inflation. Over time, global stock market returns have dramatically outpaced Inflation.

TaxPlanning – Have necessary steps been taken toward filing required business and individual tax returns, so they get filed on time? The type of business will determine the tax consequence. Tax Changes. The Tax Cuts and Jobs Act of 2017 (TCJA) lowered the corporate income tax rate from 35 percent to 21 percent.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets.

These planning opportunities are driven primarily by four factors: Materially lower market values for publicly traded securities, and a likely downturn in valuations of real estate and other illiquid assets.

So if you start with the S&P 500 or in this case stocks and bonds, you only have two asset classes, right. So the proper benchmark for those pools has to look a little bit like the underlying assets they’re investing in. If you look at the types of assets that Yale invests in, you can create a benchmark for each pool.

Like individuals, businesses holding investments and other capital assets should consider other income, gains, and losses when determining when to sell capital assets. Defer income Clients may consider putting off asset sales or delaying receipt of other income until next year to reduce 2023 taxable income.

Tax loss harvesting involves selling losing investments to offset capital gains, thus limiting the taxes you owe. While it doesn’t always make sense to take a loss on investments, evaluate your portfolio and consider whether selling some poorly performing assets may make sense in your situation. Charitable giving.

Sunset of the Tax Cuts and Jobs Act While a handful of the changes to tax law under the Tax Cuts and Jobs Act of 2017 (the TCJA) have been made permanent (such as the C corporation tax rate and the changes to the income tax treatment of alimony), many of the TCJA changes will sunset as of December 31, 2025.

Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways. From a legacy planning standpoint, two distinctions are especially important: Roth IRAs do not require their owners or spouses to take mandatory distributions.

Roth and traditional IRAs both provide tax-free growth on invested assets to account owners, but the two options also differ in a variety of ways. From a legacy planning standpoint, two distinctions are especially important: Roth IRAs do not require their owners or spouses to take mandatory distributions.

Giving and exchanging property and assets were once frequently used as a way to avoid taxes. Essentially, money-savvy wealth builders would gift and re-gift assets to shrink their tax footprint. They also used inheritances as a strategy to pass on significant wealth without paying taxes that would normally apply.

With our deep expertise and qualifications in NUA strategies, our experts are adept at navigating the complexities of tax-efficient retirement planning. Explore the Fortune Financial advantage in transforming how you manage your retirement assets and bringing you closer to achieving your financial dreams.

Morgan Asset & Wealth Management just put out their 2021 outlook. If Biden has it his way, corporations will pay more taxes than they have in the recent past. Cembalest notes, "In aggregate, Biden’s corporate taxplans would raise $2.2 Intangible asset shares were 20% in 1975, 30% in 1985 and 80% by 2005.

The “old way” – does it neglect IRMAA planning? The advisor collects the highest possible AUM fee, throws the assets into a TAMP, and then goes to play golf. Tax questions we should ponder more deeply Advisors are working on a way that is outdated when it comes to IRMAA planning. It’s time for a revamp.

Starting at the beginning of the administration in 2017. We dive deep into all sorts of things about running businesses, managing risk, and then when we began talking about his public sector service, we went deep into the Tax Cuts and Job Act of 2017. You’ve got a big asset management business that you care about.

We organize all of the trending information in your field so you don't have to. Join 36,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content